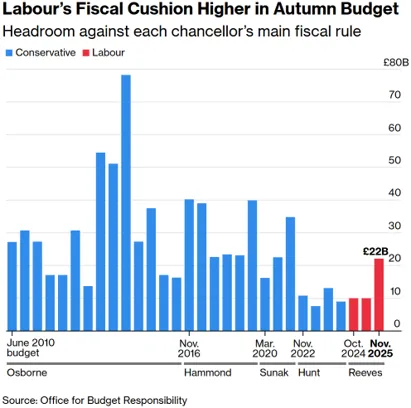

The UK Autumn Budget reassured financial markets in the short term, though structural economic weaknesses and political volatility remained unresolved

Speculation around the UK Budget - and the reaction to it - dominated the news this week, not least with the United States distracted by Thanksgiving. At heart, this was a tax‑and‑spend Budget designed to steady the UK’s finances and reassure gilt investors by creating a modest cushion of fiscal headroom. That has helped to pull gilt yields marginally lower and ease immediate borrowing pressures. Yet it leaves the UK’s deeper structural problems largely untouched. The result is an economy still locked into a low‑growth rut, ill‑equipped to fund rising demands on public services, particularly from an ageing population. For all the rhetoric about being forward‑looking, the package does little to shift the underlying pattern of stagnation.