Water and waste infrastructure businesses continue to offer attractive long-term characteristics including resilient earnings, strong cash generation and defensive growth.

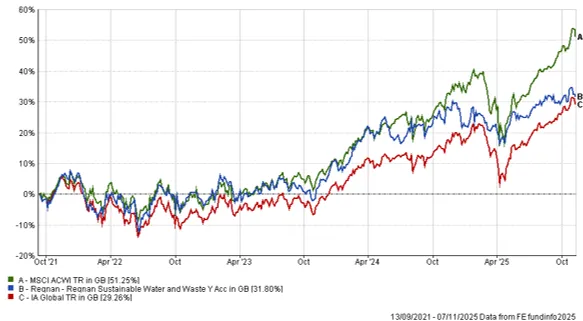

This week we caught up with Bertrand Lecourt and Saurabh Sharma, managers of the Regnan Sustainable Water & Waste Fund. This holding provides us with a targeted exposure to a corner of the real economy where earnings tend to be steady, pricing power is genuine, and competitive moats are built into the plumbing of local infrastructure. Water utilities are, by design, natural local monopolies overseen by regulators to ensure fair pricing and service quality - a structure that supports durable cash flows and underpins dividends through the cycle. In solid waste management, scale economics and route density lead to oligopolistic markets where a handful of operators set the tone on price and service, reinforcing margins and cash conversion.

A further supportive feature for the fund is the secular backdrop: governments and lenders are stepping up finance for water security just as climate volatility, ageing assets and leakage force investment. Technology also plays a part as firms digitise networks to cut losses, reduce downtime and lower energy use.

What differentiates the Regnan fund, in our view, is the way it blends both value chains - water and waste - into a high-conviction yet diversified global portfolio with low overlap to mainstream equity funds and a high degree of “purity” to its theme. That creates a resilient mix of regulated income, industrial growth and self-help efficiency stories, with competition mostly localised and barriers to entry high. Valuations are respectable relative to wider global equities and, importantly, are underpinned by consistent EPS growth and cash generation that supports dividends and future share buybacks or bolt-on M&A.

Another attraction is the fund’s low correlation to the broader equity market, particularly the technology giants that currently dominate global indices. Water and waste companies derive their earnings from regulated networks, long-term contracts and essential local services, not advertising clicks or semiconductor cycles. Over longer periods, the risk-reward profile has been notably favourable: earnings grow steadily, cash conversion is high, capital structures are sound, and the underlying need for the services scarcely fluctuates. As a result, investors are paid for their patience, with less drama along the way.