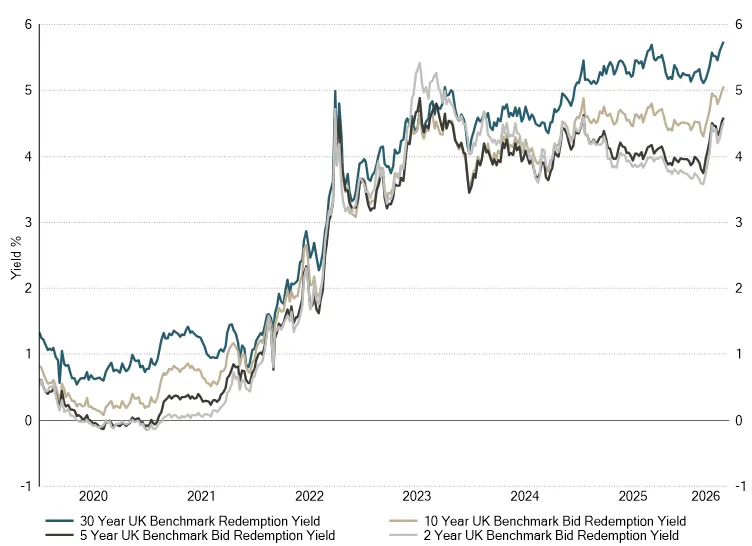

The combination of persistent inflation, rising gilt yields and political instability continued pressuring UK financial markets and reinforcing the need for diversification.

Last week's UK local elections delivered a sweeping defeat for the governing Labour party, and UK long-dated gilt yields briefly touched levels not seen since the late 1990s.

To be fair, longer-dated yields had been rising steadily ahead of polling day, driven by an energy shock since late February that has pushed UK inflation to 3.3% and which the OECD now forecasts averaging around 4% for the full year. The local election result has added a political risk premium on top: bond markets have been sensitive to any signal about the durability of the UK's fiscal framework since 2022, and the scale of Labour's losses raises questions about that durability.