The opening to 2026 has been marked by an unusually rapid pace of policy disruption emanating from the US administration. Across trade, fiscal policy, and geopolitics long-standing assumptions are being tested. Although financial markets are accustomed to political noise, the speed and breadth of recent interventions appear to have shifted up a gear.

Nowhere is this more evident than in the pressure being applied to the US Federal Reserve. Over the weekend, it emerged that the US Department of Justice has served the Fed with grand jury subpoenas relating to Chair Jerome Powell’s congressional testimony on the central bank’s headquarters renovation. Powell responded by warning publicly that monetary policy risks moving away from evidence-based decision-making toward outcomes shaped by “political pressure or intimidation.” With Powell’s term expiring in May and US President Trump signalling that any successor must support “significantly lower borrowing costs”, the independence and predictability of US monetary policy has become a growing concern for markets.

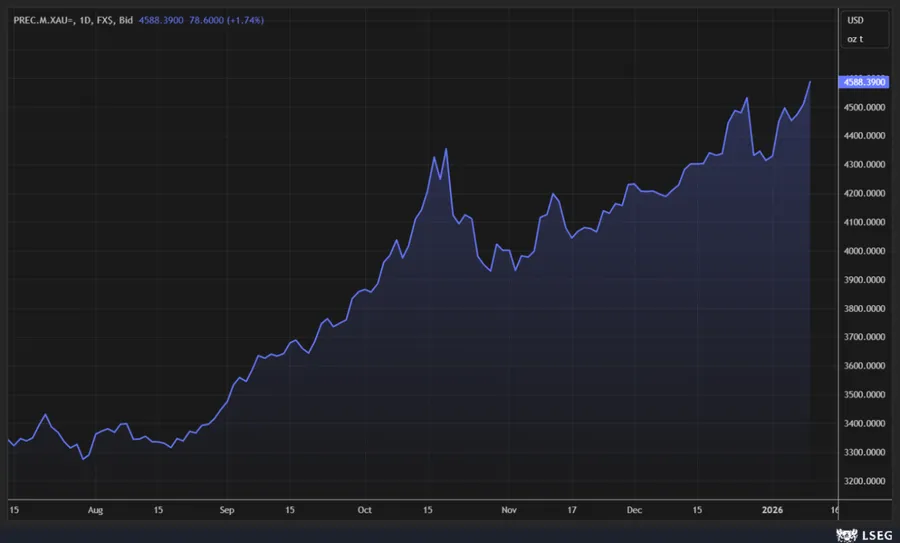

Investor reaction has been swift. Gold and silver have pushed to new highs, the US dollar has softened, and US equities have come under pressure as markets begin to price a higher risk premium into American assets - a signal that institutional uncertainty is no longer being ignored.