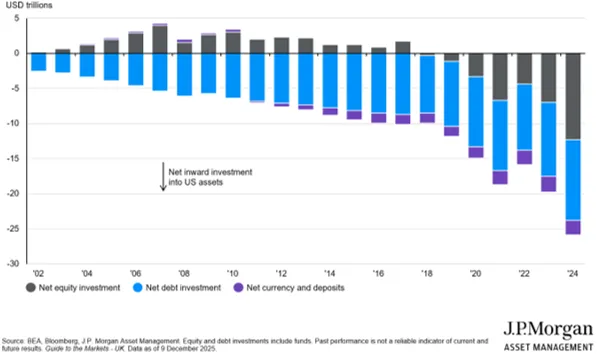

As the Bank of Japan tightens while the Federal Reserve cuts, the traditional incentive for Japanese investors and other foreign holders to buy US assets diminishes. Japanese institutions, the largest foreign holders of US Treasuries, face rising costs in managing those positions as the yen strengthens. The consequence is a shift away from liquidity expansion supporting US asset prices towards currency devaluation re-pricing assets in weaker dollars. This brings the easy era of passive 60:40 (equity:bond) investing in US assets to a close.

US Treasury yields are unlikely to fall as much as the Fed's rate cuts might suggest, as foreign demand evaporates from the long end of the curve where foreign buyers have historically concentrated their purchases. Meanwhile, the outlook for US equities is split with dollar weakness boosting reported earnings for multinational companies while valuation multiples are at risk of contracting as the “Buy American” premium erodes. In such circumstances, emerging markets and commodities become more attractive and volatility across both equity and bond markets will likely rise as this regime shift unfolds.

This would bring to an end the days of “set-and-forget” passive US equity and bond exposure. For the T. Bailey Multi-Asset Funds US Treasury exposure is modest (well below 10%) and with an effective duration of 7 years (meaning a 1% rise in yields would reduce the value of these holdings by approximately 7%), providing sensitivity to US growth expectations but less exposure to term premium and fiscal risk shocks. Instead, the funds carry greater exposure to commodities and absolute return strategies, as well as a modest hedge from US dollars to the Japanese yen.