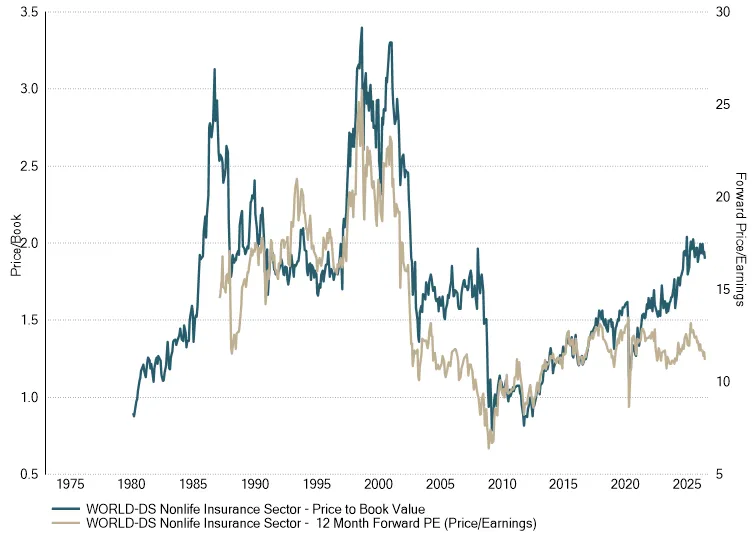

The mechanics of non-life insurance are that premiums are collected up front whilst claims are paid two to three years later. In the interim, assets are invested in cash and high-grade bonds. For much of the post-financial-crisis decade that second engine barely turned over in the era of zero interest rates. Today it operates at around 4-4.5%, contributing roughly ten percentage points to book value growth before any underwriting margin. These businesses are structurally better suited to the positive rate environment we are now in - one that, with continuing inflationary pressures, shows few signs of dissipating.

Against this more steady and mechanical generation of returns, much of the external commentary around the sector centres on property catastrophe reinsurance, where mid-year renewal pricing is down around 20% from the record levels of January 2023, after two unusually benign loss years. This describes roughly 5% of look-through premiums for the fund - near a historical low - and current pricing remains consistent with attractive returns. The buyers of that reinsurance are moreover the primary insurers that dominate the rest of the portfolio, so falling reinsurance costs reduce an input cost rather than a revenue line. Elsewhere, marine insurance has hardened following the Baltimore bridge collapse, the Middle East conflict has repriced war risk, and complex casualty is attracting mid-teens rate increases. Around 80% of look-through premiums sit in insurance lines where pricing remains supportive.

Wider concerns about private credit in financial companies are, on closer examination, largely a life insurance story outside of the focus of this fund and concentrated in private-equity-affiliated North American annuity writers with a very different liability structure. The risks that remain - principally whether catastrophe softening seeps into primary lines, or US casualty reserves prove less conservative than current data suggest - are real, but we weigh them against the structural tailwind from investment income and the discipline of current underwriting conditions.

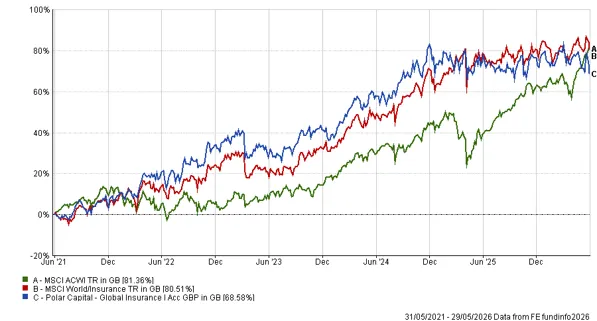

Yet perhaps the most instructive signal on the value the sector offers is what better-informed buyers are paying. Zurich's agreed acquisition of Beazley (a direct holding within the T. Bailey UK Responsibly Invested Equity Fund) was struck at a near-60% premium to its undisturbed share price and at more than twice tangible book value. The Polar Capital Global Insurance Fund’s portfolio companies are themselves repurchasing around 2% of shares per quarter. Both point to a gap between public and private assessments of the underlying economics. The case for our existing allocation to the insurance sector has not weakened during the period of recent underperformance; the valuation opportunity remains.

Compounding at mid-teens rates while the market is focused elsewhere rarely feels comfortable; it has, however, consistently proved rewarding.