The market’s “pAIn trade” accelerated as investors rapidly reassessed the long-term impact of artificial intelligence on business models and valuations.

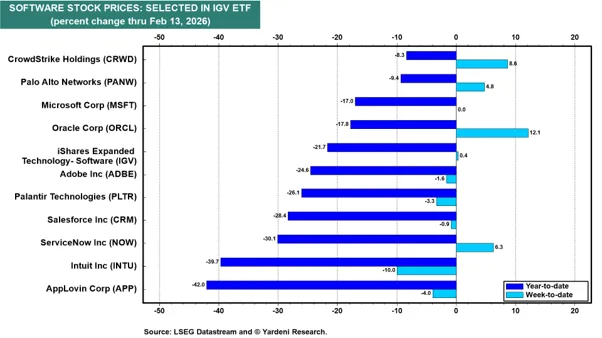

This year we’ve seen the artificial intelligence theme abruptly transition from being an unquestioned engine of equity market performance to a source of investor unease. Anxiety about AI disruption that initially focused on software has broadened into a market‑wide “pAIn trade” in which any business model perceived as vulnerable has been marked down aggressively. Software, brokerage, logistics and real‑estate‑linked stocks have all suffered sharp falls on the back of relatively limited news, as investors worry that AI‑enabled competitors could compress margins, accelerate client churn or render intermediation models obsolete. Market action has seen a “sell first, ask questions later” mentality in which a single AI headline can wipe out months of gains, even in companies that are already investing heavily in the technology themselves. This stands in contrast to the recent past, when AI was treated almost uniformly as a positive narrative and a justification for ever higher valuations across a narrow leadership group of perceived winners.

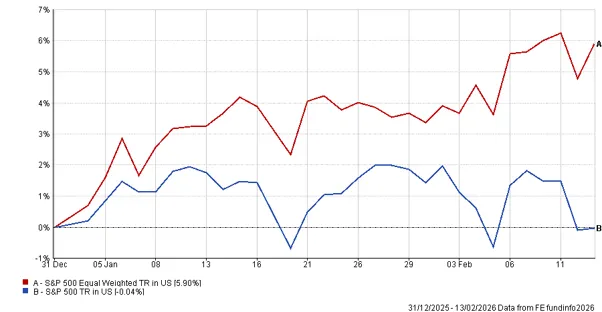

Yet, for now, this looks more like a violent rotation than an outright risk‑off episode. Headline equity indices have only modestly changed year‑to‑date, masking significant damage underneath the surface in AI‑exposed segments. Capital has been rotating out of expensive growth and AI beneficiaries and into cheaper, more traditional sectors such as financials, industrials and utilities, where AI is increasingly viewed as a potential productivity tool rather than an existential threat. This rotation has been particularly helpful for the S&P 500 equal‑weight index, which gives more influence to the broader cohort of previously neglected, lower‑valuation stocks benefiting from the shift, and less to the handful of mega‑cap AI leaders that have come under pressure.