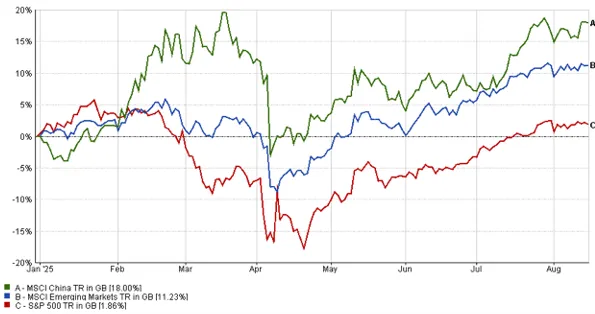

Weak Chinese economic data continued to raise concerns about long-term growth, although stimulus expectations and attractive valuations supported emerging market equities.

Recent economic data has revealed that China’s economy is losing steam. The latest numbers for industrial output, retail sales, and investment have been weaker than expected, not just in housing but now also in manufacturing and exports. China’s official growth targets look ambitious, particularly without the country addressing its deep-seated issues such as high savings rates and sluggish household spending. Nonetheless, in the shorter term, stimulus measures have been discussed which, alongside relatively attractive valuations and other factors, is helping drive the outperformance of Emerging Market equities year to date.