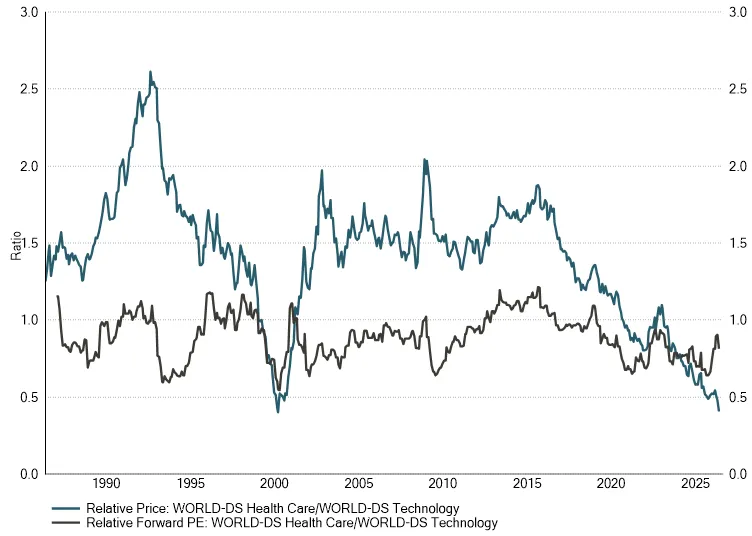

On a forward price-earnings basis, the gap between the two sectors appears modest. On a pure price basis, however, the relative-price line between the two sectors captures not just current earnings but the market's aggregate bet on long-run cash flows, earnings growth and capital allocation. On that measure, the ratio is back to levels last seen at the peak of the dot-com bubble in 1999-2000. That episode was followed by two years in which healthcare materially outperformed an unwinding technology trade. We are not in the business of forecasting precise turning points, and the AI narrative may yet have further to run before it consolidates, but we do note that the present configuration is reached only at moments of extreme dislocation, and those moments have historically rewarded having patience.

It would be easier to rationalise the de-rating if the underlying businesses were struggling. They are not. With ageing demographics, utilisation continues to grind higher, supporting revenues. New product cycles in areas such as oncology, surgical robotics and obesity care remain intact. The pressure driving this activity is structural rather than cyclical. The global pharmaceutical industry faces as much as US$300 billion of sales at risk from patent expirations by 2032, with the most acute concentration of loss-of-exclusivity events running into the early 2030s. Thus the imperative for companies to acquire late-stage biotech assets becomes strategically unavoidable. Deal premiums have remained healthy, and the small and mid-cap targets being acquired sit squarely within the most attractively valued parts of the market.

In the last week, Bristol-Myers Squibb announced a collaboration and licensing agreement with Chinese biotechnology firm Jiangsu Hengrui, covering thirteen early-stage programmes across oncology, haematology and immunology, with a US$600 million upfront payment and up to US$950 million in total near‑term payments over two years, and a potential overall deal value of up to about US$15.2 billion if all development, regulatory and commercial milestones are achieved. It is notable that an increasing share of innovation is coming from China, where drug developers can move a molecule from preclinical research to clinical-stage development in three to four years - roughly half the time the equivalent process can take in Europe or the United States. That speed advantage has historically been structural and regulatory in character; it is now being further compressed by the application of artificial intelligence to target identification, molecule design and trial optimisation. Some early studies and industry estimates suggest AI-driven efficiencies could reduce preclinical costs by 60% or more and shorten development timelines by up to 30% in their more optimistic scenarios.

The case for our existing allocation to healthcare within the T. Bailey funds has not weakened during the sector’s recent underperformance. Quite the reverse: an attractive absolute valuation, a historically extreme relative discount to technology, the most active M&A environment in years, and a fundamental backdrop largely unaffected by the AI rotation together make healthcare one of the more compelling set-ups available to us today. The trade requires patience, but the longer the rotation continues to compress healthcare valuations, the larger the eventual reversion is likely to be.

Bystanders to a boom rarely feel rewarded in the moment, but over the cycle, they often are.