Investors increasingly reassessed concentrated exposure to US assets as geopolitical leverage and policy uncertainty challenged assumptions around American exceptionalism.

Last week we wrote about the cost of uncertainty and the market’s early response to accelerating policy intervention across monetary, fiscal and geopolitical domains. Over the weekend, that uncertainty became more explicit and consequential.

The US administration’s decision to threaten escalating tariffs on multiple European allies, explicitly linked to demands around Greenland’s future status, marks yet another clear use of economic leverage in pursuit of strategic objectives. Whilst financial markets won't judge the legitimacy of those objectives, they will reassess the reliability of the institutional framework through which they are being pursued and where that appears conditional, risk premia rise.

Market signals reflect that reassessment. European defence equities have moved higher, regional currencies have experienced increased volatility, and trade relationships are being actively diversified away from reliance on the United States. Bond markets continue to price higher term premia, suggesting investor concern is shifting from near-term economic data to the stability and predictability of policy itself.

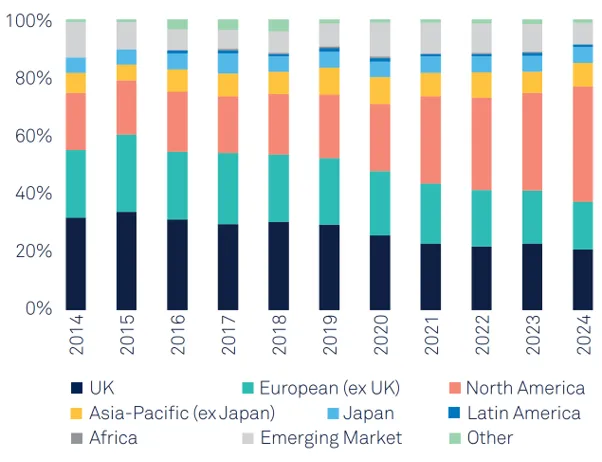

For UK investors, the implications are significant. Most multi-asset portfolios are structurally overweight the United States, with many allocating above 30% of total assets to American markets. This reflects North American equities now representing 40% of UK-managed equity portfolios - double the 20% allocated a decade ago - increasingly tracking global market-cap weights where US equities represent approximately 70% of developed indices. That positioning rests on decades of genuine American exceptionalism: deep capital markets, innovation leadership and credible institutional guardrails.

If those guardrails are perceived as negotiable, the consequences extend beyond equity valuations. Concentrated exposure to US assets creates portfolio vulnerability during periods when institutional certainty - the very foundation underpinning American financial dominance - is being tested. More diversified portfolios, with lower US concentration, thematic rather than cap-weighted equity exposure, and meaningful allocations to real assets and uncorrelated strategies, are materially better positioned to preserve capital.