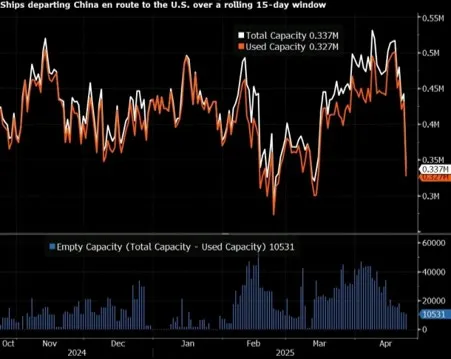

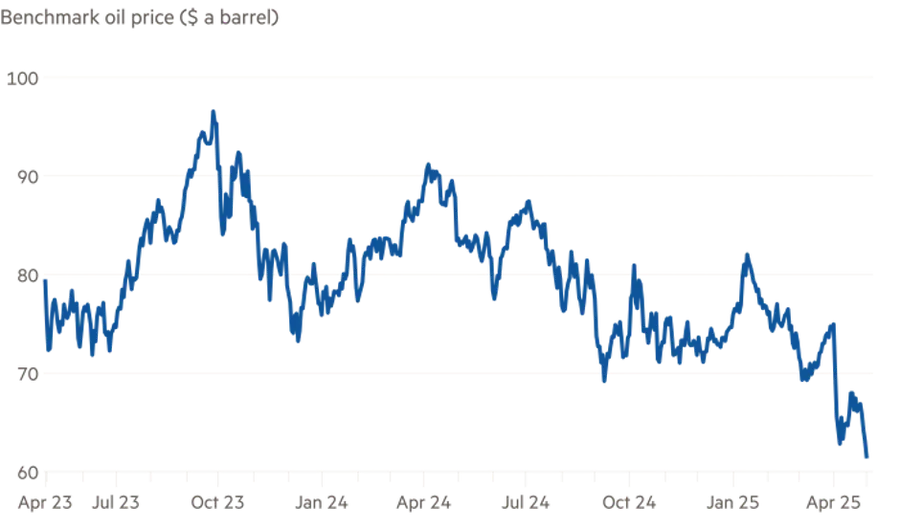

Economic data continued to show resilience, though weakening shipping activity, falling oil prices and deteriorating surveys pointed to growing downside risks.

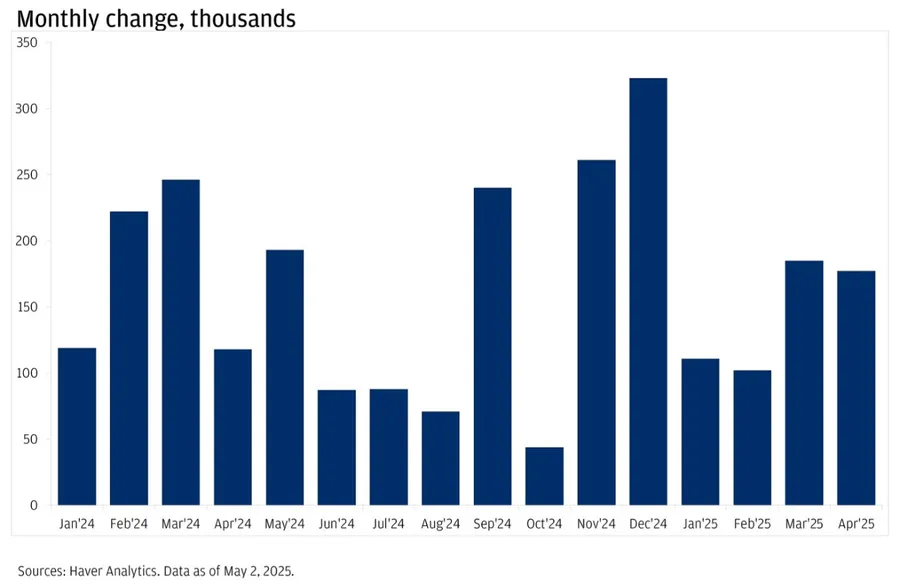

The US employment report for April released during the week was the first to cover the post-Liberation Day period and showed 177,000 non-farm payroll gains, indicating a labour market that, for now, remains in fairly good shape despite tariff concerns. Nonetheless, despite this sense of resilience, the US economy technically shrank in the first quarter as American firms sought to import goods before new tariffs hit.