It is the energy sector that serves as the primary transmission mechanism to financial markets from this conflict and whilst Brent crude has climbed to a four-month high it remains below levels a year ago and has not approached a point that would signal widespread economic disruption. The critical Strait of Hormuz, through which approximately a fifth of global oil and gas flows, remains operational despite Iranian parliamentary votes to potentially block the waterway.

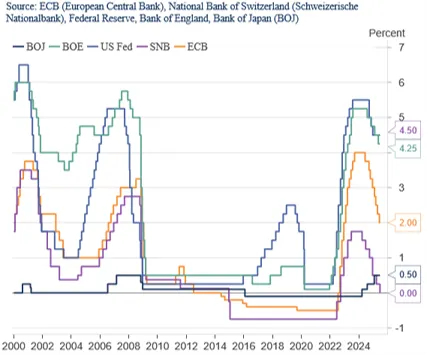

Central banks across major economies adopted a notably cautious stance this week, with scheduled monetary policy decisions reflecting the continuing delicate balance between supporting economic growth and managing inflation expectations. The US Federal Reserve maintained its benchmark rate at 4.5% while projecting two quarter-point cuts for the remainder of 2025, though updated forecasts reflected the adverse effects of recent tariff policies. The Bank of England similarly held rates at 4.25% as UK inflation remained elevated at 3.4% in May, well above the bank’s 2% target. Meanwhile, the Swiss National Bank cut rates to zero in response to deflationary pressures and franc appreciation, marking a return toward the negative rate territory it maintained from 2014 to 2022. The Bank of Japan kept rates steady at 0.5% while announcing plans to slow the pace of bond purchase reductions, signalling continued caution in unwinding its expansive monetary stimulus.