Markets stabilised temporarily following softer US rhetoric on trade, though concerns around stagflation and slowing global growth persisted.

Negative comments from US President Trump about US Federal Reserve Chair Jerome Powell along with renewed trade tensions led to sell-offs in US equities and bonds at the start of the week. However, as the week progressed, the US administration softened its stance and began hinting at possible trade deals whilst dialling down some of its harsher rhetoric. This helped markets recover somewhat with the S&P 500 ultimately rallying 4% on the week.

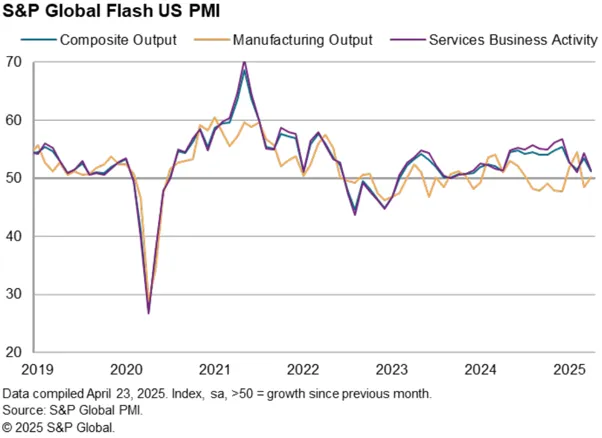

But this recovery is built on shaky ground. Recent data, including Purchasing Managers’ Index (PMI) surveys, suggest early signs of stagflation - falling output and new orders, especially in the US, alongside rising input prices. The risk of a slowdown is rising, however hard data (i.e. actual rather than survey data) will take time to come through the system.