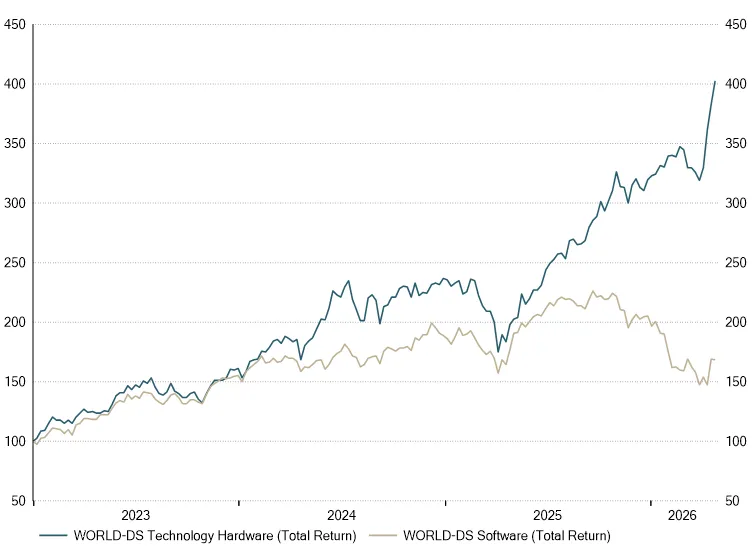

The misunderstanding that matters most concerns the addressable market for AI. For as long as the technology industry has existed, it has competed for a share of corporate IT budgets - estimated at roughly US$6 trillion per annum globally in 2026. AI is competing for something much larger: the global wage bill for knowledge workers, at approximately US$44 trillion. The implication is not that every dollar of that wage bill is immediately at risk; it is that the ceiling on the AI opportunity is of an entirely different order from anything the technology sector has previously addressed. Hyperscaler capital expenditure, which has unsettled investors accustomed to measuring technology spending against IT budgets, looks considerably less excessive when set against a prize of that size. Capital may yet prove to be poorly allocated, but the comparison sometimes drawn to the dot-com era - when fibre utilisation collapsed to 3% because the demand was simply absent - is not the right one. Compute utilisation is currently running at or above capacity, and its limiting constraint is power, not demand.

Enterprise adoption of AI has accelerated meaningfully over the past year, and the reason is less widely understood than it should be. Through 2024, benchmark scores for the most advanced AI models showed only marginal improvement in raw intelligence, which led many observers to conclude the technology had peaked. In fact, the industry's attention had shifted to reducing hallucination rates, achieved by redesigning models to reason step by step and verify conclusions before presenting them. For enterprise deployment, this matters considerably more than raw capability - a model that gives confident wrong answers is a liability whilst one that gives careful right answers becomes a tool. That shift drove the acceleration in AI revenues at the frontier model providers through the second half of 2025, and it is now beginning to appear downstream in the earnings of the companies deploying the technology.

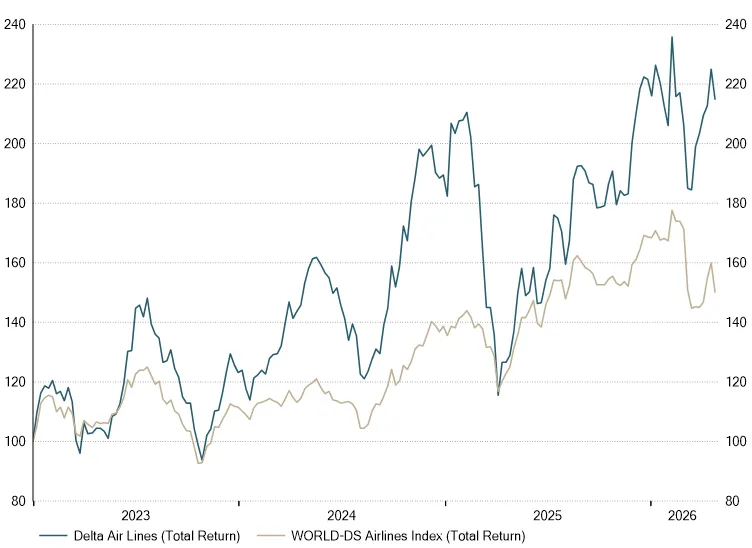

The winners, in the Polar team's view, will be the minority that have spent years quietly preparing their data infrastructure - without which the technology simply cannot function. Zhao's preferred illustration is Delta Air Lines. Uniquely among major carriers, Delta operates a single integrated system spanning ticketing, customer data and airport operations. That integration now underpins a dynamic pricing capability already visible in reported margins, and one that competitors with fragmented systems cannot replicate quickly.