This has resulted in a swift reassessment of asset prices. Gold and silver, which had seen strong inflows on the back of the debasement theme, have given back a notable chunk of their gains. Bitcoin has been hit even harder, as a crowded trade built on the idea of ever‑easier money meets the story of a Fed taking a firmer stance on inflation and balance‑sheet discipline. The US dollar, which had been on the back foot against a basket of major currencies, has stabilised and in some cases recovered.

There is a second layer to this that has compounded the move. The tentative easing of oil supply stress - with tanker flows through the Strait of Hormuz gradually recovering and Brent retreating from its highs - has taken some heat out of the near-term inflation picture. One of the market’s most acute near-term fears has faded, and with it some of the urgency behind real-asset protection.

However, the US has not resolved its long‑term debt problems. Fiscal arithmetic still points to heavy debt issuance and a growing interest bill. Low domestic savings leave the US reliant on overseas investors to help fund that borrowing, a funding backdrop that is not getting easier. Political pressure on the Fed is unlikely to have disappeared either.

The shift has been in the market’s perception of the Fed’s reaction function. Under Warsh, investors now see a central bank that may be more inclined to lean against inflation risk and less willing to underwrite a prolonged period of negative real rates. Recent commentary has also pushed markets towards pricing a tighter path for US policy than had previously been assumed, reinforcing the move higher in real yields and helping the dollar to steady.

From today’s starting point, this looks more like a reprieve for the US dollar than a full regime change. Gold’s current weakness partly explains this - some of it simply reflecting a crowded position that has been cut back now there is a clear catalyst to do so. Investors who had seen gold as a one‑directional hedge against policy error are being reminded that the asset can be volatile and that entry point and positioning do matter.

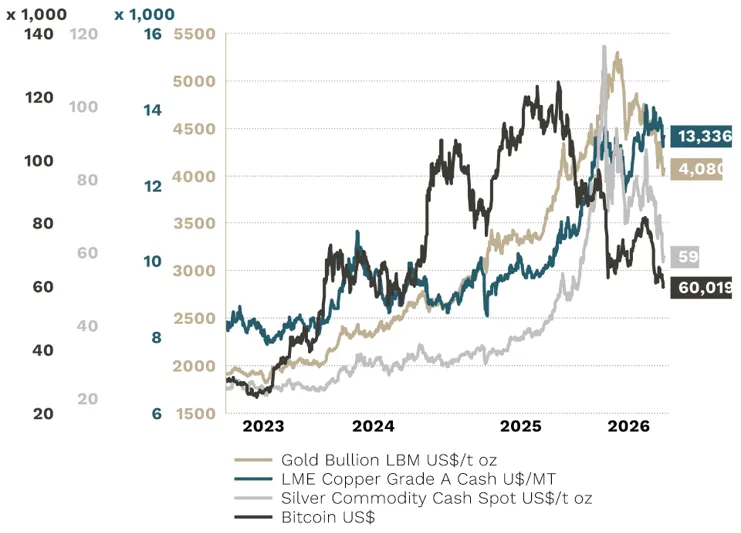

Our decision to trim gold exposure in October 2025 and again at the start of February 2026 helped reduce the T. Bailey Multi-Asset Funds’ participation in the subsequent correction, while keeping gold as a measured strategic diversifier rather than a dominant theme.

But the longer-term backdrop has not gone away. The structural arguments that fed the debasement trade in the first place remain visible: large fiscal deficits, a growing debt burden and the risk that overseas demand for US Treasuries becomes less reliable over time. If anything, Warsh’s arrival simply challenges the timing of the trade rather than erases the underlying conditions that gave rise to it.

This episode reinforces the importance of not building portfolios around a single macro story. The path is unlikely to be smooth, however persuasive it may appear at the time. Market expectations overshoot and then adjust. A diversified mix of assets that can cope with different inflation and currency outcomes remains preferable to a binary bet on one theme.

The combination of a firmer US dollar and higher real yields has implications for how specific asset classes behave, with a stronger dollar tending to tighten financial conditions at the margin, particularly for weaker borrowers outside the United States who have dollar liabilities. The equity allocations across the T. Bailey funds are already tilted towards businesses with robust balance sheets, durable cashflows and pricing power, rather than those most reliant on cheap money or a permanently soft dollar.

Gold still has a role to play as a strategic diversifier, but recent price action is a reminder that it is not a free option. In multi‑asset portfolios, exposure to gold and other real assets sits alongside a range of other diversifiers, including government bonds, credit and alternative strategies. The current drawdown in precious metals does not undermine the case for holding them over the long term as part of a broader toolkit. It does highlight the risk of treating them as an all‑weather solution to every policy concern. Gold now sits between 4% and 5% of the multi‑asset funds, which is in line with its role as a strategic diversifier alongside equities, bonds and other real assets, rather than as a dominant macro call. The dollar debasement trade has not been disproved - it is simply a reminder that markets rarely move in straight lines.