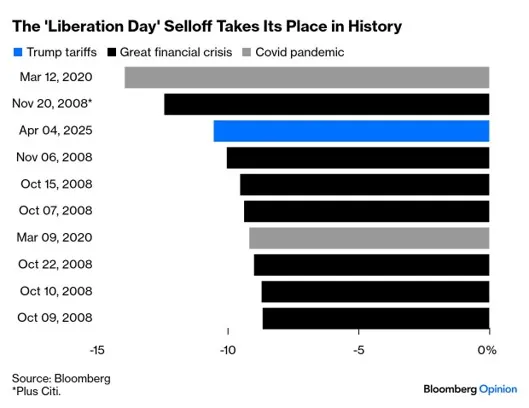

Friday’s sell-off was particularly brutal, taking the S&P 500 down over 9% for the week and pushing major indices closer to bear market territory. Technology stocks bore the brunt of the downturn, as companies like Apple and Amazon - heavily reliant on global supply chains - saw their shares tumble. Investors fled high-risk assets en masse, shifting their focus to safe havens such as US Treasury bonds and gold. The yield on the benchmark 10-year US Treasury note fell below 4%, while the gold price dipped from it's all time high but remains above $3,000 per ounce.

The tariffs represent one of the largest tax hikes in US history, effectively imposing an estimated 1.5% hit to US GDP and a 1.5% inflation impulse. These measures could severely disrupt global trade flows, exacerbate inflationary pressures, and push multiple economies into recession. JPMorgan raised its recession probability for the US and global economies to 60%, citing the ripple effects of reduced consumption and investment. Bond markets reflected growing fears of an economic downturn, with yields falling sharply as investors sought refuge in government securities.

Commodities markets were equally volatile, though performance varied across sectors. Oil prices continued their downward trajectory, with Brent crude falling to around $63 per barrel - its lowest level since 2021 - as fears of reduced global demand overshadowed OPEC production cuts.

Currency markets saw significant shifts as well. The US dollar has weakened sharply as concerns about slowing US economic growth have now overtaken trade policy as the dominant narrative in forex markets, leading to a reversal in dollar positioning. The euro has emerged as a key beneficiary of this shift, supported by fiscal reforms within Europe that have bolstered investor sentiment.

Further deterioration to risk assets now seems largely dependent on whether the tariff dispute deepens further or whether compromises with the Trump administration can be reached. Unlike other financial market downturns of recent years the US Federal Reserve will be reticent to step in unless financial stability becomes an issue. The inflationary impact of tariffs pushes back against the central bank lowering rates particularly given the instability in US tariff policy, which could look very different in the coming weeks.