The disruption in the Strait of Hormuz is increasingly feeding through to fertiliser markets, raising the risk of a prolonged and underappreciated wave of food inflation into 2027.

The energy shock has been the dominant market story for the better part of two months, and it has been written about exhaustively. The food shock that will follow it has not - yet its impact later this year and into 2027 is currently being decided in the fields, not refineries. With the Bank of England having held its Bank Rate at 3.75% last week and accepting, in notably measured language, that higher inflation is now unavoidable, the question is no longer whether UK food prices rise sharply from here but how far they go, how long they linger, and whether markets have yet begun to price them properly.

The Strait of Hormuz is well understood as a chokepoint for seaborne oil and LNG. Less appreciated is its parallel role in global nitrogen fertiliser supply. The Gulf states rank among the world's largest exporters of urea and ammonia. Qatar is a principal supplier of sulphur, a critical input in phosphate production. The disruption has already forced fertiliser manufacturers in India, Pakistan, Bangladesh and Egypt to curtail output or pay sharply elevated spot prices for LNG as feedstock. Russian and Chinese supply continues to flow, but it does not fully close the Middle Eastern shortfall. What makes this more than an input-cost story is timing. The fertiliser application window for Northern Hemisphere spring-planted crops is open right now. Where inputs are unaffordable or simply unobtainable, farmers will reduce application rates, switch to less nitrogen-hungry varieties or leave acreage fallow. That decision does not register in consumer prices for months: it comes about through lower yields, tighter grain stocks and rising feed costs before crystallising in food prices from late 2026 into 2027.

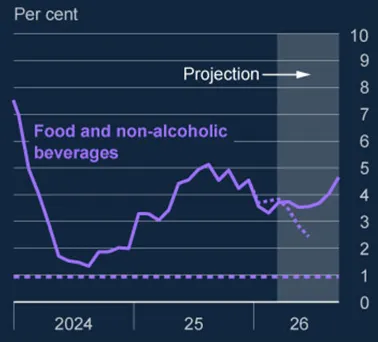

The UK inflation forecast picture has already begun to shift in response. The Bank of England's April Monetary Policy Report projected food inflation rising to around 4.6% by September, noting explicitly that fertiliser costs would push food prices "further out". The Food and Drink Federation, representing around 12,000 UK manufacturers, has revised its end-2026 forecast sharply higher to 9-10%; the Institute of Grocery Distribution models above 8% by mid-summer under its more adverse scenario. UK food inflation was running at only 3.7% in March, so even a path well below those upper bounds implies a substantial wave still to arrive. Bread, dairy and meat - the more fertiliser and feed intensive components of the basket - are likely to lead.