The effective closure of the Strait of Hormuz caused severe disruption across energy markets and raised stagflation risks for major global economies.

The situation in brief

It has been a grim week. US and Israeli forces launched coordinated strikes against Iran on 28 February, moving quickly to decapitate the regime's leadership and suppress its air defences before targeting missile production facilities and broader military infrastructure. Iran's retaliation has been chaotic and deliberately wide, striking not just US and Israeli assets but Gulf neighbours - Saudi Arabia, Kuwait, Bahrain, Qatar and the UAE - with oil facilities and civilian infrastructure caught in the crossfire. The intent appears to be to widen the conflict as far as possible.

The most consequential development came when the Islamic Revolutionary Guard Corps declared the Strait of Hormuz closed. Shipping through the Strait, which in normal times carries roughly a fifth of global seaborne oil and a substantial share of LNG flows, has effectively stopped. Qatar has shut down LNG output entirely, warning that restoring production will take weeks even once a decision to resume is made. Iraq has been forced to shut in around 1.5 million barrels per day as regional storage fills. The situation remains fluid and we are acutely conscious that behind the market moves lies enormous human suffering.

Energy and commodity markets

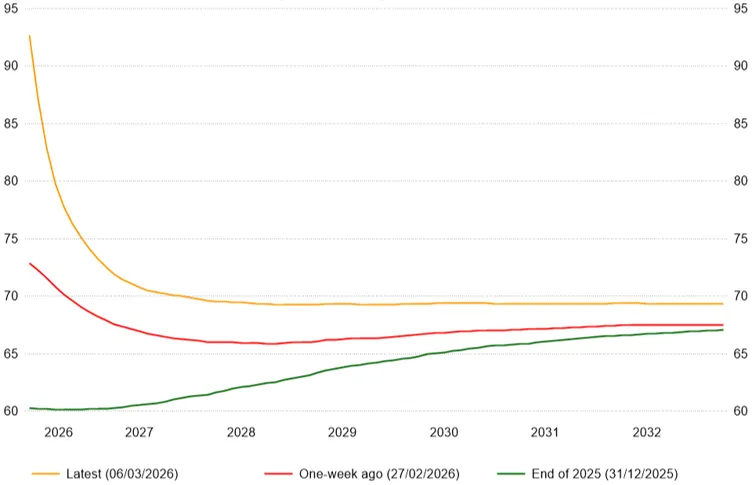

The market response has been dramatic. Brent crude, which closed last week at around US$94 a barrel, pushed above US$100 this morning (9 March 2026) - roughly 50% higher than a month ago. European natural gas has been hit harder still: the Dutch TTF benchmark has surged above €61 per megawatt-hour, nearly double its level a fortnight ago and its largest weekly gain in years.

The oil futures curve has moved into steep backwardation - the steepest since Russia's invasion of Ukraine. That structure indicates the acute near-term tightness is being priced in, but the assumption embedded in longer-dated contracts is that the disruption proves temporary. In effect, the curve is pricing a binary outcome. Either the Strait reopens in the coming weeks and prices reverse sharply, or the closure drags on for months and oil above US$100 becomes the backdrop for the rest of 2026.