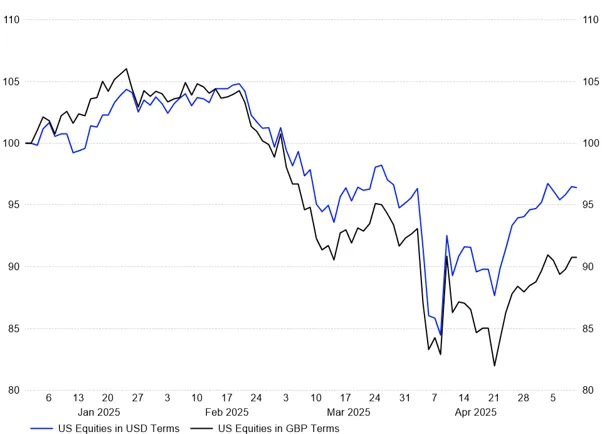

Clearly, the central narrative has been the shifting landscape of global trade policy. This week’s US-UK deal, while touted as a breakthrough, is largely symbolic, maintaining a 10% baseline tariff and offering only modest concessions. However, this sets a precedent for future trade discussions and US-China talks that commenced this weekend are expected to yield only narrow agreements.

Against this challenging backdrop, central banks have taken divergent approaches to reflect the different situations their economies face.

The US Federal Reserve held rates steady this week, expressing concern about the inflationary impact of tariffs and adopting a wait-and-see stance. The Federal Reserve’s caution reflects uncertainty about the lagged effects of tariffs on both inflation and growth, with some analysts warning that the full economic impact has yet to materialize. In contrast, the Bank of England cut rates and the European Central Bank is expected to ease policy further in response to expected disinflationary pressures.

While immediate market reactions to more encouraging trade developments have been positive and economic data has shown resilience, the underlying risks from persistent tariffs and policy unpredictability have not yet dissipated into hard data.

The risk remains that the delayed effects of tariffs could weigh on growth and keep inflation elevated, prompting central banks - especially the US Federal Reserve - to delay rate cuts longer than markets currently expect, and leaving them vulnerable to renewed turbulence if economic activity softens in the months ahead.

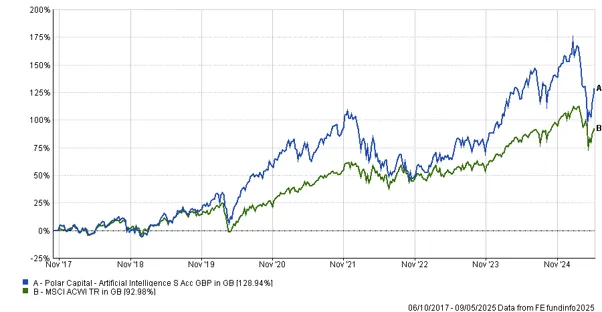

This week we caught up with Xuesong Zhao, manager of the Polar Capital Artificial Intelligence Fund. The T. Bailey funds of funds were early investors in this strategy which was established in 2017 with a forward-looking vision: to capture the transformative power of artificial intelligence as it becomes a general-purpose technology, reshaping industries in ways reminiscent of the internet and smartphones.