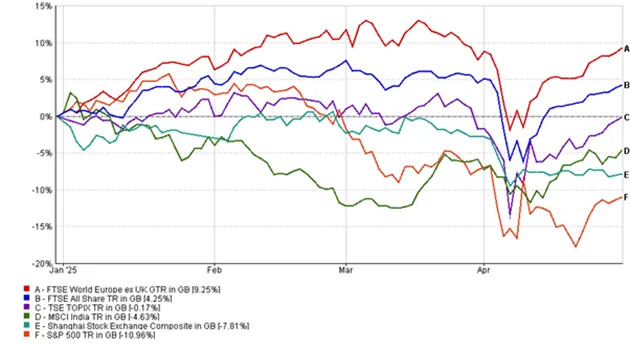

Closer to home, the FTSE 100 demonstrated relative resilience, thanks in part to its tilt towards defensive sectors and multinational exposure. Mid-cap and small-cap UK equities were more muted, reflecting their greater sensitivity to domestic and cyclical concerns.

Fixed Income: Yields Spike Then Ease

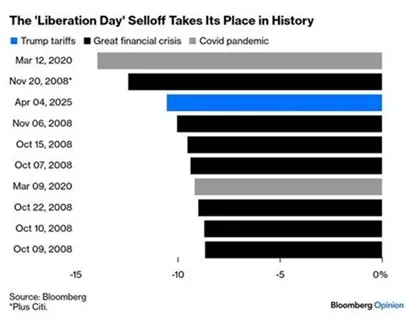

Bond markets were swept up in the broader volatility as investors initially fled US Treasuries en masse. This historic selloff resulted in a sharp rise in yields, particularly in longer-dated maturities – and ultimately appears to have been the key point of sensitivity for the Trump administration to put the brakes on their tariff rhetoric. Fortunately, as trade tensions eased later in the month, yields began to retreat. However, in contrast to equity markets, yields remain elevated compared to March levels (i.e. valuations lower).

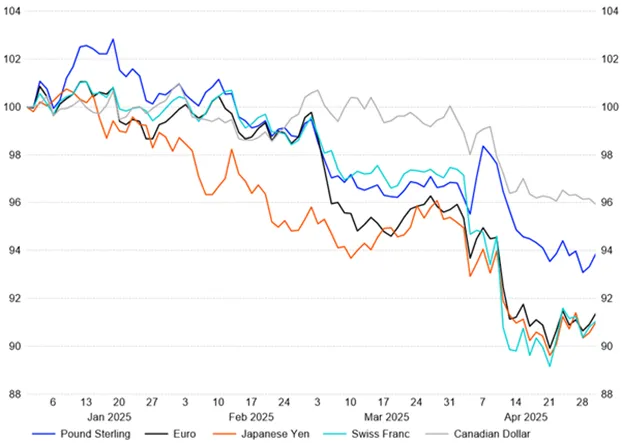

The Bank of England struck a more dovish tone in response to the global uncertainty, which helped calm the UK Gilt market by month-end. Within corporate credit, investment-grade debt saw renewed demand as Treasury yields fell, whereas high-yield bonds, particularly those linked to energy, have been under pressure.

Commodities: Diverging Fortunes

The key diversifier during this unsettling period was Gold which soared to new highs during the month as investors sought shelter from equity market turbulence and policy uncertainty. Central bank buying, particularly from China, has added fuel to the rally in recent months.

In contrast, growth-sensitive commodities came under heavy pressure. Oil prices fell sharply, driven by concerns about reduced global demand and persistent supply from US producers. Copper along with other industrial metals followed suit, reflecting the gloomier economic outlook and thus the steps taken in March to significantly reduce thematic exposure to the metal across the T. Bailey funds of funds proved well timed.

Outlook: Diversification Remains Key

With the 90-day cooling-off period underway, markets are hoping for a constructive resolution to the trade dispute. However, the calm is tenuous and any setback could see a return of volatility. Furthermore, April’s recovery in risk assets is difficult to reconcile with the sharp deterioration in sentiment and activity surveys.