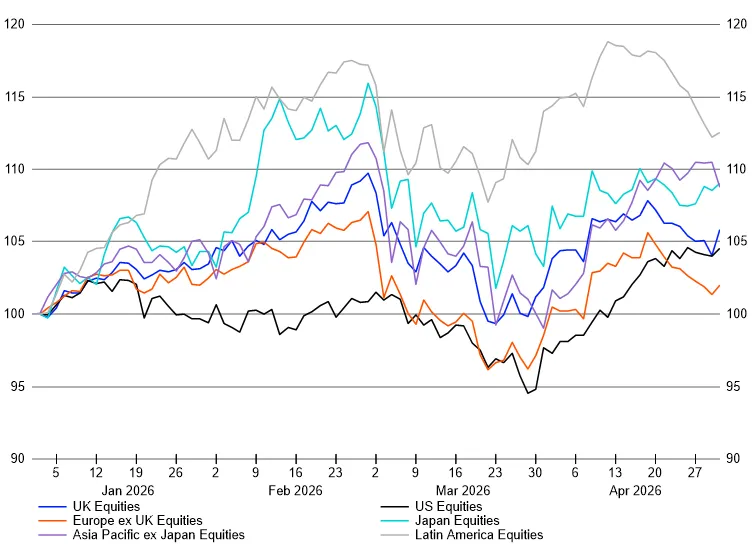

Major regional equity indices: Year to date (rebased to 100)

Source: LSEG Workspace. Total return, GBP terms

The information contained on this website is intended to provide information about our products and services and is not intended as investment advice. It is important that you do not rely upon its content to make investment decisions without seeking independent advice.

This website is intended for United Kingdom professional investors and advisers only. Please ensure you read the important legal information.

Source: LSEG Workspace. Total return, GBP terms

The AI cycle: real progress

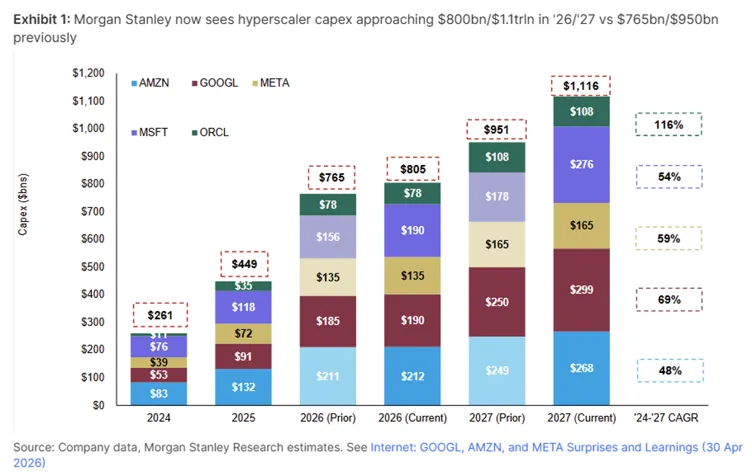

The companies that drove April’s AI rally - TSMC, Samsung, SK Hynix, and the data centre supply chain more broadly - are extraordinary businesses, but their current results are, in large part, a direct function of the capital the hyperscalers are committing. Alphabet, Amazon, Meta and Microsoft are collectively directing close to their entire operating cash flows into AI infrastructure; Meta alone has projected capital expenditure of around US$135 billion for 2026. When that level of spending flows through the supply chain, the foundries and memory manufacturers that service it will report exceptional numbers as they did.

Source: Hamilton Lane.

What those results do not yet tell us is whether the hyperscalers' investment will earn its return. The application layer - where AI's economic value to the broader enterprise economy would be most directly visible - is showing genuine green shoots. Google Cloud and AWS results offer early evidence that AI-driven enterprise adoption is accelerating. But the definitive answer to whether AI delivers the productivity transformation that justifies investment at this scale will take years, not quarters, to emerge. The dot-com parallel is an imperfect guide: even genuinely transformative technologies will suffer violent corrections when the gap between infrastructure spending and proven application-layer returns becomes too wide.

This does not make AI uninvestable - a structural argument is that AI is addressing the US$44 trillion global wage bill for knowledge workers, not merely the US$6 trillion corporate IT budget. This provides a real reason to think the ceiling on the opportunity is of a different order from anything the technology sector has previously addressed. What it does make essential is discipline about where within the AI ecosystem to invest. We feel the Polar Capital Artificial Intelligence Fund's approach - tilting towards businesses where earnings leverage is already tangible and away from those carrying the full burden of building the infrastructure - remains the right way to access the theme within the T. Bailey portfolios. Its 20.9% April return and 97.1% 12-month return reflect the compounding of that discipline over time. We remain attentive to the risk that the capex cycle that is currently powering the supply-chain trade could, in time, become its principal vulnerability.

April's internal divergence within the portfolios was stark. Holdings exposed to AI and Asia re-rated sharply; diversifiers lagged or fell. Nonetheless, the overall direction was meaningfully positive.

The clearest beneficiaries were at the Asian end of the AI supply chain. The Baillie Gifford Pacific Fund returned 19.5% - recovering much of its sharp March losses as Korean and Taiwanese equity markets surged to record highs on AI memory and foundry demand. The Lansdowne (Lux) Developed Markets Fund returned 13.0%, comfortably ahead of the broader IA Global sector, and JK Japan returned 8.0%, outperforming the TOPIX by approximately 3 percentage points and extending a compelling multi-year track record.

Within emerging markets, the picture was more mixed. Whilst the HSBC MSCI Emerging Markets ETF broadly tracked the very strong EM index, the Merlin Fidelis Emerging Markets Fund lagged by approximately 8.5% - its active positioning, which served investors well in March, worked against it in April as the rally concentrated almost entirely in Korean and Taiwanese semiconductor names the fund holds in deliberately limited size. The team's 12-month return of approximately 52% - comfortably ahead of its peer group - reflects the longer-term record we continue to back. WS Zennor Japan Equity Income similarly lagged the IA Japan sector at 1.2%, its value- and income-oriented approach not designed to lead in a month defined by a single technology earnings theme; its longer-term record and its differentiated positioning within Japan remain intact.

The defensive thematic strategies produced results consistent with their purpose in the T. Bailey portfolios: Polar Capital Healthcare Opportunities returned 1.5%, Regnan Sustainable Water and Waste 3.2%, WS Havelock Global Select 2.8% and Ranmore Global Equity 2.1% - none of these strategies would be expected to lead in months dominated by AI capex beneficiaries, and each retains a clear role within the broader portfolios. Polar Capital Insurance fell 1.9%, with specialty reinsurance names proving sensitive to revised claims estimates related to energy and supply-chain disruption - a position we continue to monitor closely.

IP Group returned 16.5% as improved risk appetite lifted the university-spinout universe. Chrysalis Investments continued its recovery, returning 7.0%, with the three-year wind-down structure now providing a clearer pathway to capital return; Starling Bank, which accounts for the majority of net asset value, continues to build operational momentum, and the shares remain at a material discount to NAV.

Among the diversifiers, gold was the most significant drag. The iShares Physical Gold ETC has been weak throughout the Hormuz crisis. Higher oil prices and war-related inflation have kept expectations for interest-rate cuts in check and real yields elevated. That combination has weighed on gold even in an environment where its safe-haven credentials might have been expected to shine. Nonetheless, the same ETC has returned approximately 37% over the past 12 months, and the structural demand from emerging-market central banks deliberately diversifying away from US dollar reserves has intensified through the conflict. Gold, held at around 5% in the multi-asset funds, remains a conviction position. The AQR Adaptive Equity Market Neutral UCITS strategy returned -4.4%; factor-based approaches are structurally challenged when a single earnings-driven theme dominates across sectors simultaneously, and we are reviewing its contribution in the context of the broader absolute return allocation. Man Absolute Value (+3.7%) and TM Fulcrum (+1.3%) both contributed modestly and positively, as did Man High Yield Opportunities and the Barings Emerging Markets Debt Blended Fund, where tightening credit spreads rewarded the positions.

With energy prices elevated, central banks holding firm and growth being revised down, the instinct to reach for the 2022 playbook - sell bonds, sell growth equities, brace for rate hikes - is understandable. Just over half of professional asset allocators surveyed by Bank of America in early April expected stagflation as their base case. We continue to think this is a misdiagnosis.

The 2022 shock involved prices accelerating at their fastest pace in forty years against a backdrop of genuinely resilient demand, with central banks so far behind the curve that markets had to price in aggressive tightening almost overnight. What is happening now is structurally different: inflation is persisting rather than accelerating, and it is doing so against a global economy with already fragile demand. In the UK, households face mortgage rates above 5% and the prospect of energy bills rising again in July; the domestic growth outlook is weak before the energy shock's full effects have been felt. This distinction matters for fixed income. The Bank of England's recent decision to hold at 3.75% reflects a genuinely trapped Monetary Policy Committee. All else being equal, if growth disappoints as materially as the OECD's revised 0.7% UK forecast for 2026 suggests it will, rate expectations will ultimately have to fall back.

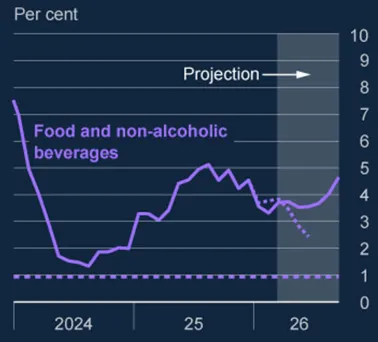

The energy shock has been dissected exhaustively, and the oil futures curve already embeds an assumption of gradual price normalisation through 2027. The food shock that will follow it has attracted far less attention - yet for investors in the T. Bailey Multi‑Asset funds, whose long‑term objective is to grow capital ahead of inflation, it may prove at least as important.

The Strait of Hormuz is well understood as a chokepoint for oil and LNG. Less appreciated is its wider role in other industries such as global nitrogen fertiliser supply. The Gulf states rank among the world's largest exporters of urea and ammonia; Qatar is a principal supplier of sulphur, critical for phosphate production. Manufacturers across South and Southeast Asia have already been forced to curtail output or pay elevated spot prices for LNG as feedstock. The fertiliser application window for Northern Hemisphere spring-planted crops is open now. Where inputs are unaffordable or unavailable, farmers will reduce application rates, switch varieties, or leave land fallow - a decision that does not register in consumer prices for months, arriving instead via lower yields, tighter grain stocks and rising feed costs before crystallising in food prices from autumn 2026 into 2027.

The Bank of England’s April Monetary Policy Report already projects UK food inflation rising to around 4.6% by September, explicitly noting that fertiliser costs will push prices “further out”, while industry forecasts for 2026 point considerably higher. UK CPI was running at only 3.3% in March. A second, food‑led wave of inflation would therefore land just as markets are pricing a fading energy impulse and a resumption of rate cuts. From the perspective of the T. Bailey Multi‑Asset funds’ objectives, that implies a more prolonged period in which inflation remains a live headwind to be outpaced rather than a spike that quickly recedes.

Dotted line: February 2026 projection.

Dashed line: 2012-2019 average.

Source: Bank of England Monetary Policy Report April 2026

Food inflation also behaves differently from energy. Energy prices tend to overshoot and then retrace as supply responds over multi-year horizons. Food inflation is stickier, driven by physical supply deficits that take a growing season to correct, and it is structurally more regressive: lower-income households spend a materially larger share of their budgets on essentials, so the economic and political pressure persists long after Brent crude retreats. For investors seeking to compound ahead of inflation, that points towards assets with genuine pricing power over input costs, real assets linked to agricultural supply chains, and a cautious approach to interest-rate risk as the baton passes from energy to food.

The T. Bailey portfolios are broadly positioned for this: short-to-medium duration bonds that avoid the duration a persistent food inflation wave would punish; thematic equity exposure to healthcare, water and infrastructure where demand is largely non-discretionary; value-oriented equity strategies with genuine pricing power over input-cost pressures. A diplomatic breakthrough in the coming weeks may tempt investors to temper their inflation concerns alongside a fall in oil prices. We think that would be premature.

Across energy, food and AI, the narratives will keep changing; the constant for the T. Bailey funds is a disciplined, diversified approach that looks through individual stories and stays focused on long-term real outcomes for investors.