Diverging central bank policies and commodity extremes defined December. Investors questioned the long-term returns from AI investment.

The Regime Shift Unfolds

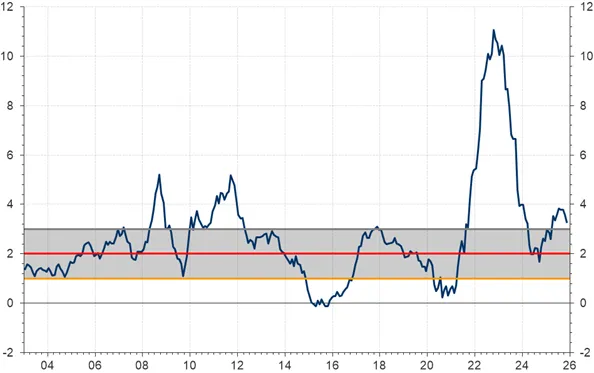

The month began with the US Federal Reserve delivering its third rate cut of 2025, lowering its policy rate range to 3.5%-3.75% following softer inflation data - headline CPI cooled to 2.7% in November - alongside evidence of softening labour market conditions.

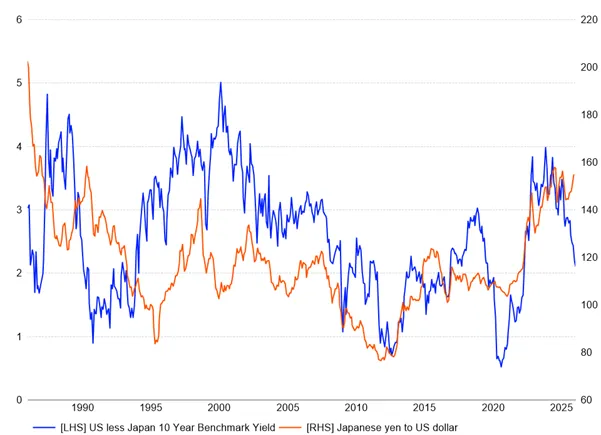

Just one week later, the Bank of Japan raised its policy rate to 0.75%, the highest level in three decades. This move represents a deliberate step away from the ultra-accommodative monetary stance that has characterised the Japanese economy for the better part of two decades. In doing so, it strengthens the case that the long-running "US dollar supercycle" - underpinned by superior US interest rates may be approaching its limits.

In the UK, the Bank of England cut its benchmark rate by 25bps to 3.75%, albeit the narrow 5-4 vote revealed division within the Monetary Policy Committee. Four members preferred to hold rates steady, highlighting continued concerns over persistent wage growth and service-sector inflation despite a weakening growth backdrop.

The Dollar's Loss, Emerging Markets' Gain

To some extent, the divergence in monetary policy has already begun to reframe currency and capital flow dynamics. As Japanese institutions - historically among the world's largest holders of US Treasury securities - face rising costs in managing their US dollar exposures whilst yen strength accelerates, the incentive to continue accumulating US assets has diminished materially. Nonetheless, while the US dollar broadly weakened in December, it has appreciated over recent months relative to the Japanese yen as fiscal sustainability concerns have weighed on both economies.