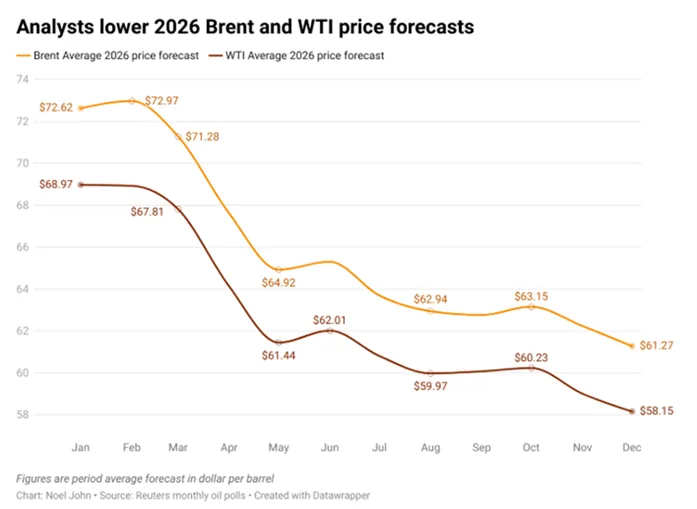

Brent and WTI prices declined by approximately 19% and 20% respectively during 2025, their sharpest annual falls since 2020, largely due to production increases from OPEC. Saudi Arabia alone increased production by roughly one million barrels per day over the course of the year.

According to OPEC’s most recent monthly report, global oil supply and demand are expected to be closely balanced in 2026, with both projected at approximately 106–107 million barrels per day.

On the demand side, it is worth noting that forecasters such as the International Energy Agency have softened their long-standing “peak oil demand” thesis. A slowdown in global electric vehicle adoption has contributed to expectations that oil demand will continue growing through to at least 2030.

When viewed relative to other commodities, oil appears particularly depressed. At current prices, one ounce of gold buys around 80 barrels of oil. This ratio has only been exceeded once in the past 35 years, during the brief period in 2020 when oil prices turned negative at the height of the Covid pandemic.

Given the prevailing bearish consensus, it is worth considering an alternative perspective. Goehring & Rozencwajg (G&R), a specialist natural resources investment firm, have recently argued that oil may be poised to take over the leadership baton from gold. The firm was notably constructive on gold three years ago and now sees a similar opportunity emerging in oil markets.

Their thesis highlights the extremely negative sentiment surrounding oil, reflected in the bearish price targets outlined above. G&R argue that oil is widely perceived as obsolete and structurally challenged, leading to significant under-ownership. The energy sector now accounts for approximately 4% of the S&P 500, compared with over 10% a decade ago.

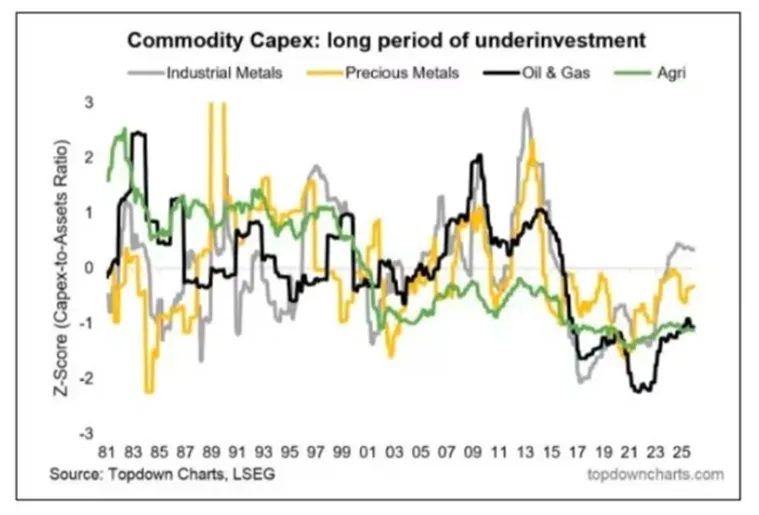

G&R contend that when investor pessimism becomes sufficiently extreme, capital investment dries up. In such an environment, supply can no longer respond adequately to demand, ultimately driving prices higher. The chart below illustrates how periods of sustained under-investment are historically unsustainable.