AI entered a more selective phase while energy risks increased. Emerging markets continued to lead performance.

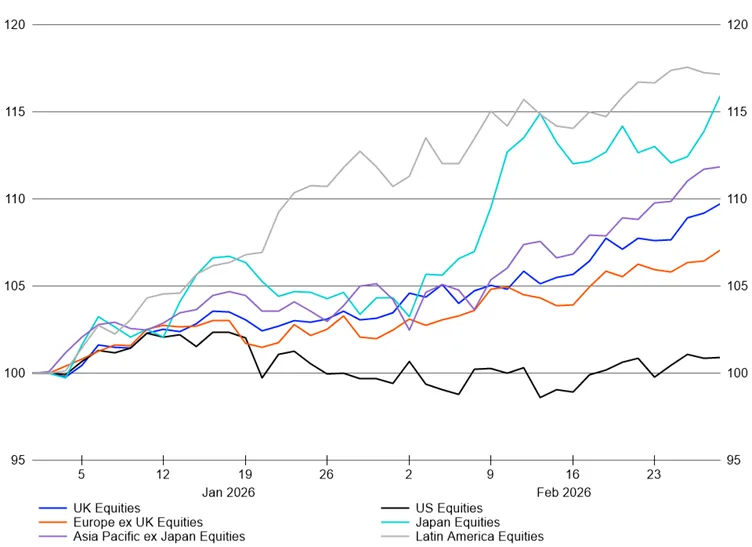

Global equities delivered another positive month in February, with leadership continuing to broaden beyond the narrow US mega-cap theme of recent years. Asia and emerging markets led the way into the month-end, even as late-month geopolitical shocks and renewed AI volatility reminded investors why diversification across regions and styles matters. More recent weakness at the start of March underlines that leadership in these markets is unlikely to be in a straight line.

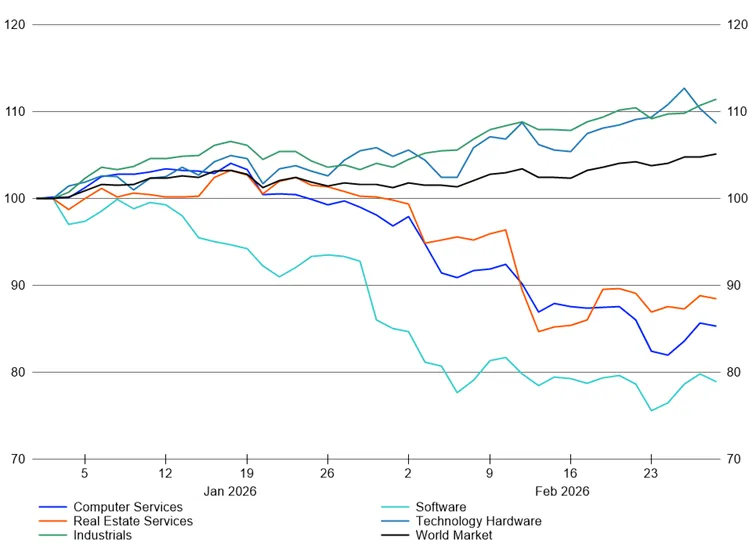

February saw the artificial intelligence theme shift from being an unquestioned engine of equity market performance to a source of unease, as investors reassessed who really captures the economics of automation. The immediate trigger was Anthropic’s launch of industry specific plugins for its Claude Cowork tool - notably in law, finance and other document heavy workflows - which crystallised fears that general purpose AI agents could erode the value of established software franchises and data platforms.

Enterprise software, legal tech and information services names suffered sharp, often double-digit declines on relatively limited company-specific news, as markets adopted a “sell first, ask questions later” stance towards anything perceived as being vulnerable to AI disintermediation. The pressure extended beyond pure software into segments such as brokerages, logistics and real estate linked business models, where AI-enabled process automation and price transparency are seen as potential margin and volume threats. At the same time, the “picks and shovels” side of AI - notably semiconductors, data centre infrastructure and selected hardware enablers - remained better supported by capex commitments and robust earnings upgrades.

Within the T. Bailey funds, this environment rewarded a restrained approach that treats AI as an important but contained theme rather than one permitted to dominate portfolios. The Polar Capital Artificial Intelligence Fund, held across the T. Bailey funds of funds, continued to add value through its tilt towards beneficiaries of the technology whilst avoiding the most vulnerable, high multiple software-as-a-service (“SaaS”) names. In contrast, the First Trust NASDAQ Cybersecurity UCITS ETF (held in the T. Bailey Global Thematic Equity Fund) and idiosyncratic growth exposure via Chrysalis Investments (held across the fund of funds’ portfolios) detracted, as both were caught in the wider derating of richly valued growth and private market assets. In Chrysalis’s case, lingering governance and mandate uncertainty compounded the sector-level pressure.

We believe markets are moving into a more discriminating, bottom-up phase of the AI cycle. The easy gains from broad thematic exposure look largely behind us; from here, stock-level judgement about individual business models and competitive positioning will matter far more than simply owning the theme.