Institutional uncertainty drove capital shifts. Emerging markets outperformed while gold benefited from safe-haven demand.

January was shaped less by economic data and more by events that challenged the institutional foundations underpinning asset allocation. The US Department of Justice’s criminal investigation into Federal Reserve Chair Jerome Powell - relating to congressional testimony on the central bank’s headquarters renovation - prompted Powell to warn publicly of “political pressure or intimidation” aimed at influencing monetary policy. Three former Federal Reserve Chairs and a number of global central bank governors responded with coordinated statements defending central bank independence.

At the same time, the US administration threatened escalating tariffs - rising from 10% in February to 25% by June - on eight NATO allies, explicitly linked to demands regarding Greenland’s future status. The European Union openly discussed activating its Anti-Coercion Instrument regulation, while France warned that Europe would not “passively accept the law of the strongest”.

These were by no means conventional trade disputes, but deliberate use of economic tools to pursue strategic geo-political objectives. With frameworks that markets have assumed to be structural beginning to appear conditional on political progress, investors have started to reassess their reliability and to demand higher compensation for uncertainty.

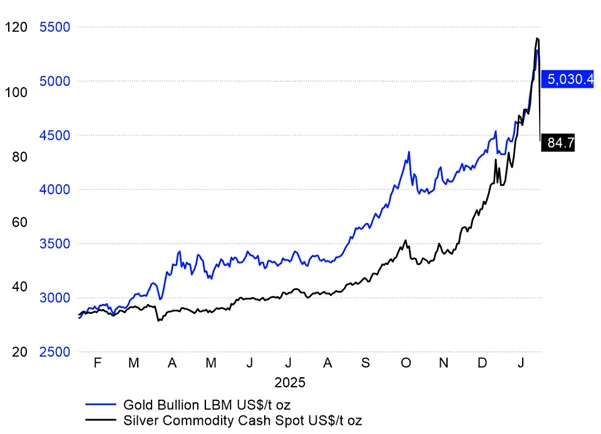

The market response was to push the price of gold on further, beyond US$5,000 per ounce and the US dollar to a four-month low as currency markets repriced risk, and equity leadership rotated decisively away from US mega-cap technology towards Asia and emerging markets.

For UK investors, many of whom remain structurally anchored to US assets, weakening of institutional certainty - long a cornerstone of American financial dominance - has material implications for portfolio construction. In this context, concentration risk transitions from being a feature of “US exceptionalism” to an identifiable portfolio weakness to address.