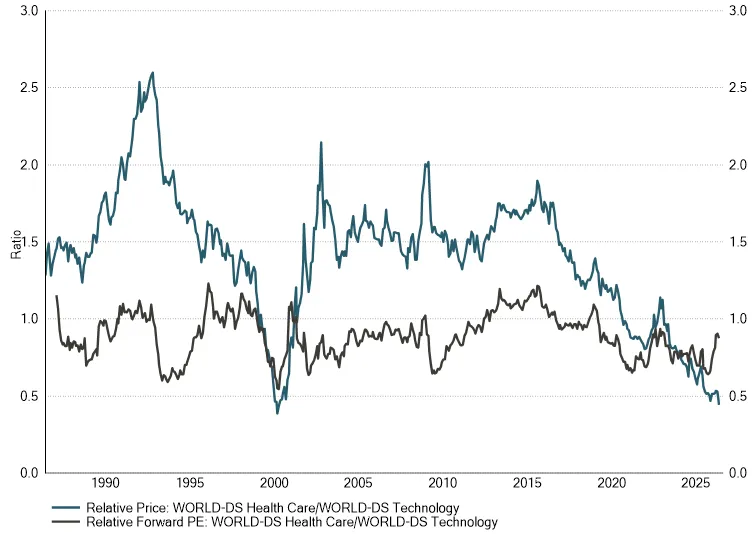

It would be easier to rationalise this if the underlying healthcare businesses were struggling, but they are not. The month closed with a sharp illustration of the disconnect between scientific achievement and market recognition. At the ASCO (American Society of Clinical Oncology) annual meeting in Chicago, the full data from testing of a new drug, daraxonrasib, in pancreatic cancer reportedly received a standing ovation from more than 9,000 oncologists. The drug doubled median overall survival compared with chemotherapy, from 6.7 months to 13.2 months, in a disease where meaningful progress has been elusive for decades. Alongside that, Novo Nordisk's oral Wegovy received European approval, and Bristol-Myers Squibb announced a collaboration with Jiangsu Hengrui covering thirteen programmes, with up to US$15.2 billion in potential milestones - one transaction in what is the most active pharmaceutical M&A environment in years. The case for our allocation to healthcare has not weakened during its relative share price underperformance. Bystanders to a boom rarely feel rewarded in the moment, but over the cycle, they often are.

Similar logic applies to other themes within the T. Bailey funds. For the Regnan Sustainable Water and Waste Fund, it is business as usual: steady margins, consistent cash flows, and quiet compounding. US industrial production and construction activity were both rising through the month - a direct volume catalyst for waste businesses. And there is a connection between the AI infrastructure build driving the equity market and the businesses inside this fund that the market has not yet begun to price: data centres are significant consumers of water, creating structural long-duration demand for businesses the market is currently content to ignore. Strong assets out of favour because attention has moved elsewhere. The AI trade requires the narrative to remain intact, sentiment to remain elevated, and earnings to continue surprising to the upside. The water and waste case requires only that the businesses continue doing what they have always done.

How the portfolios fared

The AI theme and Asian equities drove the month's positive results. The Polar Capital Artificial Intelligence Fund returned 10.9%, extending its twelve-month return to +98.0%; the First Trust NASDAQ Cybersecurity ETF returned an astounding +32.1%; and the Baillie Gifford Pacific Fund rose 15.4% as Samsung crossed the US$1 trillion market capitalisation on AI memory demand. The Lansdowne (Lux) Developed Markets and JK Japan funds were both strong performers. Following the strong run in each, we trimmed our positions in the Polar Capital Artificial Intelligence Fund (in the Global Thematic Equity and Multi-Asset Growth funds) and Baillie Gifford Pacific Fund (in the Global Thematic Equity Fund).

The Merlin Fidelis Emerging Markets Fund lagged - the mirror image of its outperformance in March, when the same deliberate underweighting of the AI hardware trade protected investors in a month of indiscriminate selling - its twelve-month return remains well ahead of its peer group. Among the diversifiers, gold gave back a little of its safe-haven premium and copper rose meaningfully on AI infrastructure demand and improving industrial activity. Chrysalis Investments fell sharply, adding to a frustrating run despite its wind-down structure being in place, Starling Bank's operational momentum remaining intact, and its shares sitting at a deep discount to net asset value.

Looking ahead

Our base case remains a gradual yet bumpy resolution of the Hormuz crisis. But a reopening of the Strait is only the beginning of normalisation and not the end of the disruption. Infrastructure rebuilds on a physical timeline; food prices follow a seasonal one; political systems adjust on their own terms, which are rarely convenient.

The equity market is extended: concentration is at historic extremes, the equity risk premium is close to zero, and a large wave of index-eligible supply - SpaceX, OpenAI, Anthropic - is about to land. The capital to absorb it will need to come from somewhere, and the most natural sources are the areas that are most crowded. Against that backdrop, assuming that strong growth themes continue unabated - and building portfolios as if they will - strikes us as unwise. The AI investment cycle is real and we maintain meaningful exposure to it, but the T. Bailey funds are constructed to generate returns across a range of outcomes, not to depend on any single narrative remaining intact. That means holding healthcare businesses generating genuine medical breakthroughs at historically cheap valuations; water and waste businesses compounding quietly through the noise; diversified emerging market exposure not reducible to the semiconductor trade; and real assets providing ballast against an inflation story that has further chapters to run. Our trimming of AI positions this month, following their exceptional run, reflects that discipline in practice.

Investment returns over a full cycle have rarely come from the most crowded part of any market. They have tended to come from the parts the market was too distracted to look at carefully, and that is where much of our attention is focused.