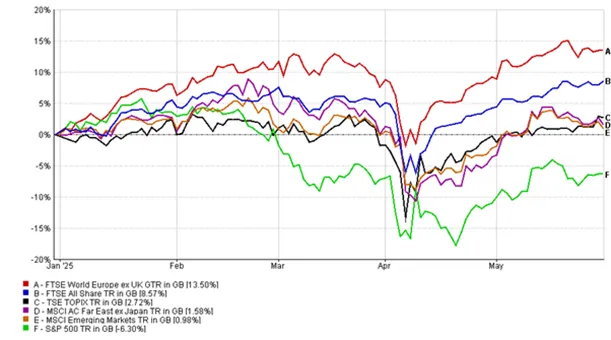

It is notable, however, that for sterling-based investors the US equity gains in May were muted by ongoing dollar weakness, leaving the US equity market’s returns in negative territory year-to-date in GBP terms. The dollar extended its decline, pressured by softening US growth data, policy uncertainty, and trade disruptions that saw first-quarter GDP contract. Meanwhile, European equities performed better than global peers, supported by the ECB’s dovish stance and a proposed €500 billion defence spending package that supports manufacturing and security sectors.

Your Money

This month we trimmed US exposure across the T. Bailey Funds of Funds portfolios through a partial sale of the iShares S&P500 Equal Weight UCITS ETF. As we continue to further diversify equity exposure we introduced a position in the newly launched Merlin Fidelis Emerging Markets Fund.

This fund differentiates itself by employing a disciplined, research-driven approach to emerging market stock-picking focussing on businesses with strong competitive advantages and with valuations that provide a strongly favourable risk-reward opportunity. The managers adopt a flexible approach without preset style, sector, or country biases, remaining receptive to opportunities wherever they may emerge. This research-driven methodology is further enhanced by a rigorous peer review system, ensuring that each investment thesis undergoes comprehensive evaluation before being added to the portfolio.

In the T. Bailey Multi-Asset funds, we also reduced our holding in Urban Logistics plc. The share price has exhibited strong performance since LondonMetric Property plc's initial bid for the company in April, with Urban Logistics achieving a year-to-date return of 56% by the end of the month.