The AI theme continues to dominate global equity markets, but soaring valuations and increasingly concentrated market leadership are raising important questions for investors. This week's update explains why T. Bailey has been reducing exposure to the AI theme while continuing to believe in its long-term potential.

This week we have seen the end of the 2nd quarter, and as investment managers, it is a time when we assess the winners and losers in our funds over that period. Perhaps unsurprisingly, the areas of the market that have been very strong over the quarter have been companies exposed to the AI narrative. For example, the US Semiconductors index was up 88% over the quarter, driven by earnings momentum that is forecast to grow by ~100% this year. The current weighting of US Semiconductor companies in the S&P 500 is ~19% versus 2% in 2015. This AI trade phenomenon is not unique to the US, as can be seen by the performance of both the Taiwan and South Korean markets returning 45% and 67% respectively over the quarter.

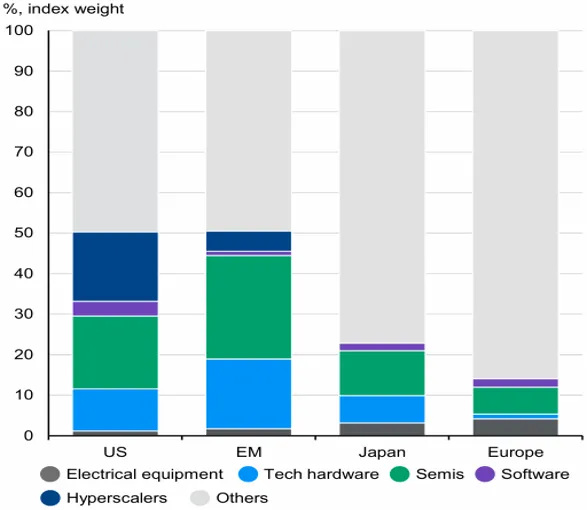

It is worth noting the inter-correlation of the “AI trade” across regions, as can be seen in the chart below from JP Morgan, and how concentrated certain markets are to it. This is an important observation that certainly passive investors should be aware of, as they may believe that they are diversified by region, but unaware that their greatest factor exposure risk is to the AI trade, given the concentration risk in some regional markets.