Volatility returned as AI sentiment shifted. Diversification across asset classes supported portfolio resilience.

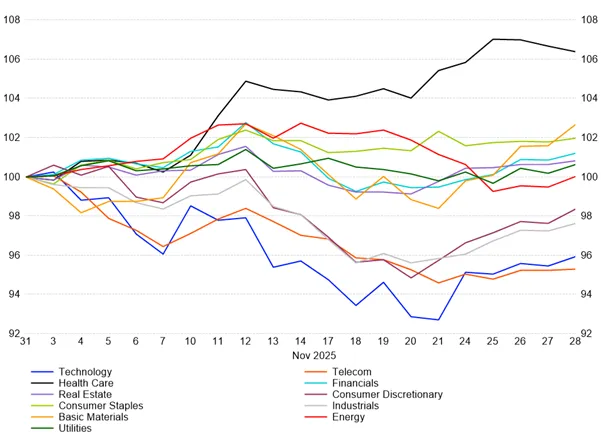

November was a largely flat month overall for investors following a long stretch of gains earlier in the year. It was not without volatility however as a combination of the resolution to a record US government shutdown, delayed economic releases and a sharp correction in technology related shares exposed crowded areas of the market, particularly in AI‑linked names. Equities lost momentum, technology and AI‑linked shares saw sharp moves in both directions and government bonds and other diversifiers started to earn their place in portfolios again. The construction of the T. Bailey funds of funds has this in mind: not to seek to eliminate volatility, but to temper it within a range commensurate with longer-term return objectives and to ensure that no single investment story - however enticing in the short term - dominates the performance outcome.

In equity markets, while AI remained the centre of attention, focus has been shifting from excitement over its growth potential to concerns over how it is funded and how sustainable that is. OpenAI, the creator of ChatGPT and a name synonymous with the theme, has spoken on sizeable infrastructure agreements over the coming years that add up to well over US$1 trillion with Oracle, Broadcom, Nvidia, AMD and Amazon. Such numbers underline how capital‑intensive AI has become. They also explain why investors are asking harder questions about who will ultimately earn an acceptable return on all this spending, and who’s balance sheets are carrying the risk. In the T. Bailey funds of funds, this environment reinforces our approach of maintaining exposure to the AI theme mainly via a specialist manager and sizing the exposure sensibly within a broader set of other themes and regional exposures - avoiding any one technology cycle dictating the overall risk profile.

That discipline showed its value as technology and AI‑exposed stocks corrected through much of the month. High‑profile short positions in the market in names such as Palantir and Nvidia, together with concerns about stretched valuations, triggered meaningful falls in the Nasdaq and other growth‑heavy indices. At the same time, more income‑generating and less cyclical parts of the market - including healthcare, insurance and quality dividend‑paying companies - held up relatively well.