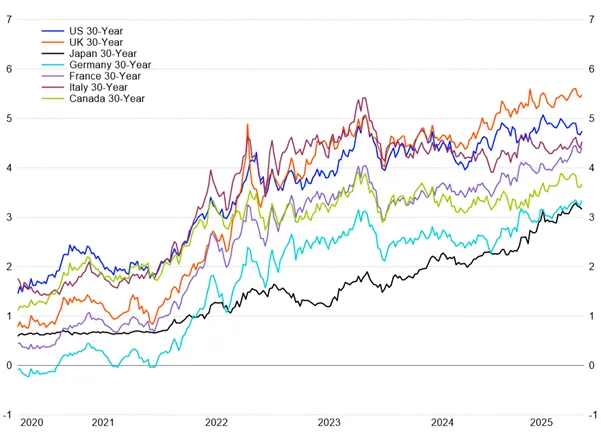

At the shorter end of the government bond yield curve, the US Federal Reserve delivered its first rate cut of 2025, lowering the target range by 25 basis points to 4.00–4.25%. Fed Chair, Jerome Powell, described the move as risk management, citing weaker labour demand and moderating household spending. Stephen Miran, attending his first policy meeting as a new governor favoured by the Trump administration, dissented for a 0.5% cut and projected faster easing into year-end. Justification was evident in the labour market as August payrolls rose just 22,000 against 75,000 expected, June was revised to show a loss of 13,000, and longer-term revisions removed 911,000 jobs from the March 2024–March 2025 period. However, US inflation pressures remain persistent, pulling the US Fed in opposite directions.

The European Central Bank and Bank of England opted to hold rates steady. The ECB kept its deposit rate at 2% as eurozone inflation edged up to 2.1%. The Bank of England left its rate at 4% albeit slowed its pace of quantitative tightening.

The US closed September with a government shutdown, furloughing 750,000 federal employees after Congress failed to pass a budget. President Trump announced 100% tariffs on imported branded pharmaceuticals from 1 October, alongside duties on selected furniture and trucks, while also pressing TikTok’s forced sale.

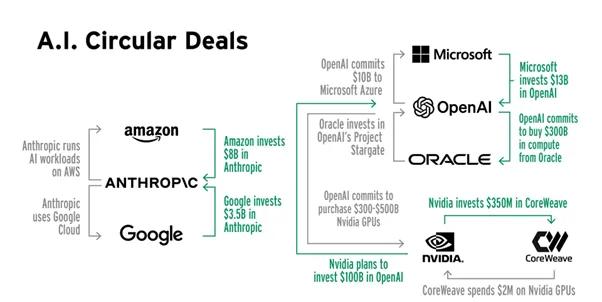

Equity markets continued to be dominated by the artificial intelligence theme. Nvidia pledged up to US$100 billion to finance OpenAI’s future hardware orders. While this secures revenue to Nvidia in the short term, it ties Nvidia’s growth to a partner that’s not expected to be cash-flow positive before 2029. History offers clear warnings in this regard where telecom suppliers in the late 1990s and General Electric in the 2000s used similar vendor-financing models that ultimately collapsed when customers defaulted.