Global markets were rocked in April as the Trump administration ratcheted up trade tensions between the US and the rest of the world, igniting fears of a slowdown in global growth. The month began with a jolt as US President Trump unveiled sweeping tariffs on imports, branding the move “Liberation Day”. The announcement triggered sharp selloffs across risk assets, with US equities falling heavily, industrial commodities tumbling, and bond yields spiking.

S&P 500 index’s 10 greatest two-day selloffs this century

Source: Bloomberg, 7 April 2025.

Remarkably, financial markets regained composure mid-month following the introduction of a 90-day pause to allow for trade negotiations.

Thus, overall, the US equity market as measured by the S&P 500 closed down for the month by just 0.7% in US dollar terms, with technology stocks leading the rebound. Companies like Apple and Microsoft, part of the so-called “Magnificent Seven”, erased losses from early in the month as investors anticipated their ability to adapt supply chains and maintain pricing power despite trade barriers.

Unfortunately, the outcome for non-US based holders of US equities was quite different as the whole trade policy debacle has been characterised through a “selling America” narrative that weighed on the US dollar.

US Dollar in Decline

US Dollar relative to other currencies, rebased to 100 at 31 December 2024.

Source: LSEG Workspace.

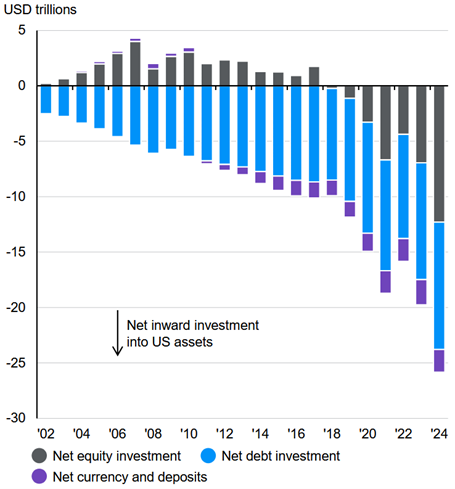

A story of US exceptionalism has been in play for many years now, and has seen savings disproportionally allocated to US assets, reducing the cost of capital for US companies and elevating their valuation multiples, both in absolute terms and relative to other markets.

US Net International Investment Position

Source: JP Morgan Asset Management Guide to the Markets, 30 April 2025.

The US administration’s new trade policy destabilises this regime and brings into focus the attraction of other international markets. Whether this escalates further into a de-dollarisation trend remains to be seen. Nonetheless, it is notable that during this period of financial market stress the US dollar has been regarded anything but a safe-haven.

Equities: Rebound Follows Initial Shock

Generally, international markets have offered a more constructive picture so far in 2025, particularly those less in the tariff firing line.

Regional equity performance

Source: FE Analytics. Total return, GBP terms.

Closer to home, the FTSE 100 demonstrated relative resilience, thanks in part to its tilt towards defensive sectors and multinational exposure. Mid-cap and small-cap UK equities were more muted, reflecting their greater sensitivity to domestic and cyclical concerns.

Fixed Income: Yields Spike Then Ease

Bond markets were swept up in the broader volatility as investors initially fled US Treasuries en masse. This historic selloff resulted in a sharp rise in yields, particularly in longer-dated maturities – and ultimately appears to have been the key point of sensitivity for the Trump administration to put the brakes on their tariff rhetoric. Fortunately, as trade tensions eased later in the month, yields began to retreat. However, in contrast to equity markets, yields remain elevated compared to March levels (i.e. valuations lower).

The Bank of England struck a more dovish tone in response to the global uncertainty, which helped calm the UK Gilt market by month-end. Within corporate credit, investment-grade debt saw renewed demand as Treasury yields fell, whereas high-yield bonds, particularly those linked to energy, have been under pressure.

Commodities: Diverging Fortunes

The key diversifier during this unsettling period was Gold which soared to new highs during the month as investors sought shelter from equity market turbulence and policy uncertainty. Central bank buying, particularly from China, has added fuel to the rally in recent months.

In contrast, growth-sensitive commodities came under heavy pressure. Oil prices fell sharply, driven by concerns about reduced global demand and persistent supply from US producers. Copper along with other industrial metals followed suit, reflecting the gloomier economic outlook and thus the steps taken in March to significantly reduce thematic exposure to the metal across the T. Bailey funds of funds proved well timed.

Outlook: Diversification Remains Key

With the 90-day cooling-off period underway, markets are hoping for a constructive resolution to the trade dispute. However, the calm is tenuous and any setback could see a return of volatility. Furthermore, April’s recovery in risk assets is difficult to reconcile with the sharp deterioration in sentiment and activity surveys.

US Consumer Confidence (Conference Board)

Source: LSEG Workspace.

US New Orders Index (Philadelphia Federal Reserve)

Source: LSEG Workspace.

As risks are skewed to the downside and much depends on unpredictable policy developments we continue to favour a selective, broadly diversified stance across the T. Bailey portfolios and from here are minded to take opportunities to reduce risk.

Shorter-duration bonds remain useful in managing interest rate risks, while selective exposure within credit could provide attractive income returns. Gold remains a potential hedge against geopolitical and currency uncertainty, though position sizing remains key as some pullback after its sharp gains might be expected.