Key Market Insights

Central bank divergence: The Bank of Japan lifted rates to 0.75% in December whilst the US Federal Reserve and Bank of England both cut. This policy decoupling has the potential to unwind decades of capital flows that have favoured US assets.

Commodity rally reached extremes: Gold surged to record highs above US$4,500 per ounce and silver approached US$72, reflecting safe-haven demand, currency weakness and expectations of further monetary easing across developed markets.

Artificial intelligence concerns deepened: Amidst ongoing capital expenditure commitments, investors are increasingly questioning whether investment in AI infrastructure is outpacing near-term revenue generation.

UK economic momentum stalled: Soft growth in Q3 2025, coupled with rising unemployment and cooling inflation, reinforced the case for further interest rate cuts but raises ongoing questions about underlying structural challenges to UK growth.

The Regime Shift Unfolds

The month began with the US Federal Reserve delivering its third rate cut of 2025, lowering its policy rate range to 3.5%-3.75% following softer inflation data – headline CPI cooled to 2.7% in November – alongside evidence of softening labour market conditions.

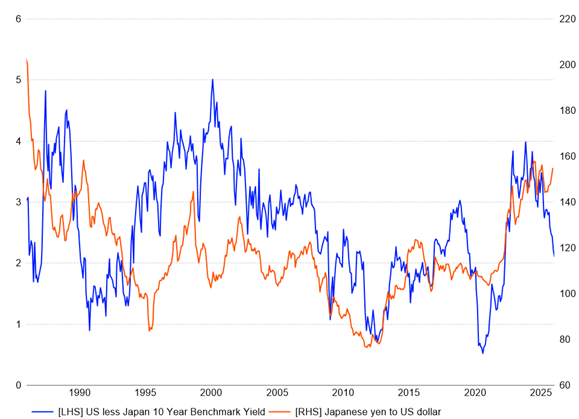

Just one week later, the Bank of Japan raised its policy rate to 0.75%, the highest level in three decades. This move represents a deliberate step away from the ultra-accommodative monetary stance that has characterised the Japanese economy for the better part of two decades. In doing so, it strengthens the case that the long-running “US dollar supercycle” – underpinned by superior US interest rates may be approaching its limits.

In the UK, the Bank of England cut its benchmark rate by 25bps to 3.75%, albeit the narrow 5-4 vote revealed division within the Monetary Policy Committee. Four members preferred to hold rates steady, highlighting continued concerns over persistent wage growth and service-sector inflation despite a weakening growth backdrop.

The Dollar’s Loss, Emerging Markets’ Gain

To some extent, the divergence in monetary policy has already begun to reframe currency and capital flow dynamics. As Japanese institutions – historically among the world’s largest holders of US Treasury securities – face rising costs in managing their US dollar exposures whilst yen strength accelerates, the incentive to continue accumulating US assets has diminished materially. Nonetheless, while the US dollar broadly weakened in December, it has appreciated over recent

months relative to the Japanese yen as fiscal sustainability concerns have weighed on both economies.

Japanese yen exchange rate with the US dollar alongside longer-dated interest rate differentials

Source: LSEG Workspace.

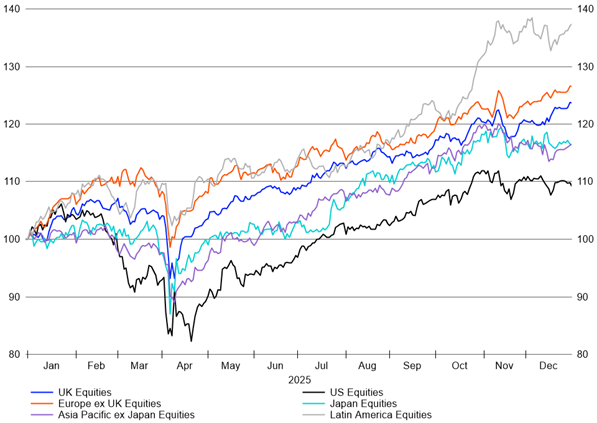

More broadly, shifts in relative interest rate expectations and currency trends have favoured non-US assets during 2025. Emerging market equities, having already gained 26.7% in 2025 – their strongest performance since 2017 – continued to attract inflows.

Regional equity returns in GBP terms for 2025

Source: LSEG Workspace. Total return, GBP terms.

The traditional US-centric 60:40 portfolio – 60% equities, 40% bonds – has long been the default allocation for passive investors. However, with longer-dated US Treasury yields remaining elevated due to fiscal pressures and waning foreign demand, whilst non-US assets benefit from relative monetary easing and a weaker US dollar, the foundations of global asset allocation appear to be shifting.

For the T. Bailey funds of funds, portfolio positioning reflects this evolving backdrop. The T. Bailey Multi-Asset Funds retain exposure to commodities and absolute return strategies that serve to enhance diversification and provide broader opportunities in a world of heightened policy divergence. Additionally, a relatively low US dollar exposure alongside selective emerging market exposure provides participation in the reshaping of global capital flows whilst limiting reliance on the dollar-denominated assets that have dominated the last two decades.

The Profitability Question for Artificial Intelligence

Artificial intelligence remained the defining investment theme of 2025, yet it now raises the question of whether the scale of capital expenditure required to build artificial intelligence infrastructure is outpacing future revenue generation and returns on that capital.

A mid-month profit warning from Oracle, which revealed weaker-than-expected cloud revenue growth, raised fresh questions about customer appetite for AI services. Subsequent news that Blue Owl Capital had withdrawn from Oracle’s US$10 billion Michigan data-centre project added to concerns around infrastructure economics. Oracle shares tumbled over 15% during the month, marking the company’s worst quarter since 2001, dragging broader AI-adjacent sectors lower.

Whilst the longer-term AI narrative remains intact – large language models demonstrating increasing capability, enterprise adoption expanding, and long-term productivity gains appearing credible – investors are now asking more searching questions about where value ultimately accrues.

The UK’s Persistent Growth Challenge

UK economic news remained challenging. The Office for National Statistics reported marginal growth of just 0.1% in the third quarter of 2025. Unemployment rate rose to 5.1% in the three months to October, the highest level since January 2021, with youth unemployment (ages 16-24) climbing to 16%, its worst reading in over a decade. Wage growth, whilst still elevated on an annual basis at 4.6%, eased further and was increasingly concentrated in the public sector, where pay rises announced in 2025 were phased in.

Inflation, however, continued to cool. The consumer price index fell to 3.2% in November, well below expectations and providing justification for the Bank of England’s December rate cut. Yet the combination of subdued growth and lingering inflation – what some have termed “stagflation-lite” – leaves policymakers constrained.

UK CPI and the Bank of England target rate

Source: LSEG Workspace.

This paradox creates opportunity for investors. UK equity valuations remain materially lower than those of US and European peers, and dividend yields more attractive than those available from many other developed markets. Even in an environment of subdued domestic growth, UK equities continue to offer relative value for long-term investors.

Safe Havens and Commodity Extremes

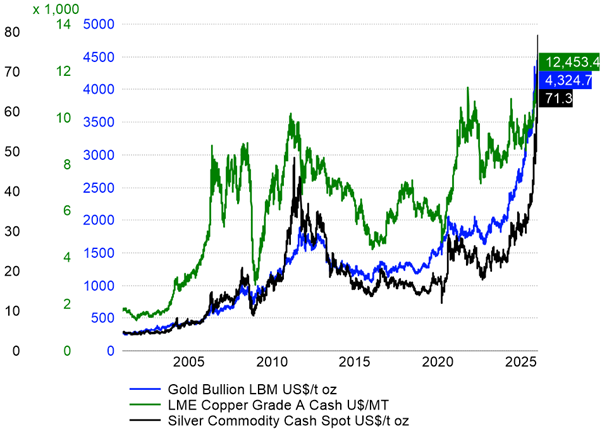

December saw two of the most precious commodities – gold and silver – reach extraordinary valuations. Gold surged past US$4,500 per ounce, delivering a 65% return for the year, whilst silver struck a nominal record high near US$72 per troy ounce, up 144% in 2025. These moves reflected a convergence of safe-haven demand, currency debasement concerns and expectations of further monetary easing.

Copper also reached an all-time high of US$11,540 per tonne in early December, driven by supply constraints and depleted warehouse inventory. This rally, driven by optimism about long-term electrification and energy transition trends, has offset concerns about near-term demand weakness in China.

Gold, Silver and Copper Prices

Source: LSEG Workspace.

For T. Bailey’s multi-asset portfolios, commodity exposure remains strategic. Beyond their inflation hedging role, commodities have again demonstrated their value as diversifiers during periods when both equities and traditional bonds face headwinds. Allocations to gold and copper reflects both our long-term thematic conviction (energy transition, population growth, urban development) and near-term tactical considerations (currency weakness, monetary policy divergence).

Portfolio Positioning

Looking to the year ahead, portfolio construction across the T. Bailey funds of funds reflects the structural uncertainties outlined above, with an emphasis on:

- Selective US exposure: acknowledging valuation risk and the erosion of the “Buy American” premium

- Commodity and inflation hedges: addressing both structural long-term themes and near-term policy-driven volatility

- Geographic and thematic diversification: ensuring no single narrative or regional exposure dominates outcomes

- Flexible bond exposure: prioritising credit selection over duration

- Absolute return and alternative strategies: providing resilience when traditional correlations shift

As 2025 draws to a close, the dominance of a singular market narrative – whether US exceptionalism or unchallenged AI optimism – has given way to a more nuanced market environment. The limits of the US dollar cycle, the emergence of legitimate questions about AI profitability, persistent UK stagnation and widening central bank policy divergence are collectively reshaping the investment landscape.

For long-term investors, these transitions, whilst potentially unsettling in the short term, create opportunities. The repositioning of global capital from US dollar assets to alternatives, the discipline required to value artificial intelligence investments at reasonable multiples, and the opportunity to access UK and emerging market assets at valuations that offer genuine risk-return appeal. These all underscore the benefits of a diversified, unconstrained and thematically informed approach to investing.

The T. Bailey funds of funds are constructed with these principles in mind – seeking multiple sources of return and maintaining flexibility – positioning the portfolios to adapt as economic and market conditions evolve.