A More Discerning Phase for AI

Gulf tensions drive an energy shock: Late‑month escalation in the US-Israel conflict with Iran pushed oil prices sharply higher and triggered a classic risk‑off response, with government bonds and gold finding support and equities – particularly in Asia at the start of March – coming under renewed pressure.

Asia and emerging markets ahead, but tested: Global equities rose in February, with Asia and emerging markets again outperforming while US indices were relatively stable, even as volatility picked up beneath the surface and, in early March, spilled over into a sharp regional sell-off.

AI enters a more discriminating phase: A sharp rotation away from richly valued AI linked software and “disruption risk” business models towards cheaper, more traditional sectors underlined that investors are now questioning where the long-term economics of AI will truly accrue.

Diversification continues to earn its keep: February saw the T. Bailey Multi-Asset and Global Thematic funds extend their strong start to 2026, supported by deliberate tilts towards Asia and emerging markets and a discerning approach to powerful long-term themes.

Global equities delivered another positive month in February, with leadership continuing to broaden beyond the narrow US mega-cap theme of recent years. Asia and emerging markets led the way into the month-end, even as late-month geopolitical shocks and renewed AI volatility reminded investors why diversification across regions and styles matters. More recent weakness at the start of March underlines that leadership in these markets is unlikely to be in a straight line.

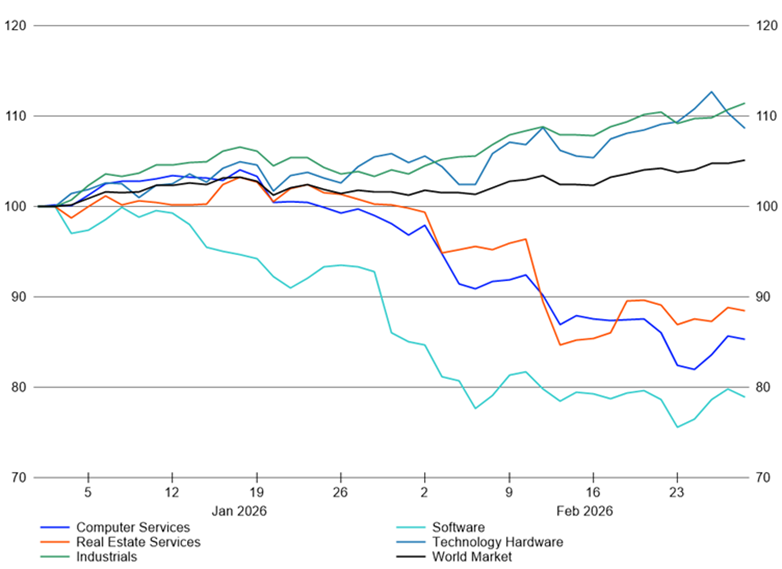

February saw the artificial intelligence theme shift from being an unquestioned engine of equity market performance to a source of unease, as investors reassessed who really captures the economics of automation. The immediate trigger was Anthropic’s launch of industry specific plugins for its Claude Cowork tool – notably in law, finance and other document heavy workflows – which crystallised fears that general purpose AI agents could erode the value of established software franchises and data platforms.

Enterprise software, legal tech and information services names suffered sharp, often double-digit declines on relatively limited company-specific news, as markets adopted a “sell first, ask questions later” stance towards anything perceived as being vulnerable to AI disintermediation. The pressure extended beyond pure software into segments such as brokerages, logistics and real estate linked business models, where AI-enabled process automation and price transparency are seen as potential margin and volume threats. At the same time, the “picks and shovels” side of AI – notably semiconductors, data centre infrastructure and selected hardware enablers – remained better supported by capex commitments and robust earnings upgrades.

Within the T. Bailey funds, this environment rewarded a restrained approach that treats AI as an important but contained theme rather than one permitted to dominate portfolios. The Polar Capital Artificial Intelligence Fund, held across the T. Bailey funds of funds, continued to add value through its tilt towards beneficiaries of the technology whilst avoiding the most vulnerable, high multiple software-as-a-service (“SaaS”) names. In contrast, the First Trust NASDAQ Cybersecurity UCITS ETF (held in the T. Bailey Global Thematic Equity Fund) and idiosyncratic growth exposure via Chrysalis Investments (held across the fund of funds’ portfolios) detracted, as both were caught in the wider derating of richly valued growth and private market assets. In Chrysalis’s case, lingering governance and mandate uncertainty compounded the sector-level pressure.

We believe markets are moving into a more discriminating, bottom-up phase of the AI cycle. The easy gains from broad thematic exposure look largely behind us; from here, stock-level judgement about individual business models and competitive positioning will matter far more than simply owning the theme.

Selected World Equity Sectors: Year-to-date

Source: LSEG Workspace. Rebased to 100 at 31 December 2025. Total return in GBP terms.

For much of February, macro data remained broadly supportive of risk assets. US growth indicators pointed to cooling but not collapsing activity; Eurozone inflation drifted closer to target, and Japanese wage and export data reinforced a constructive domestic backdrop.

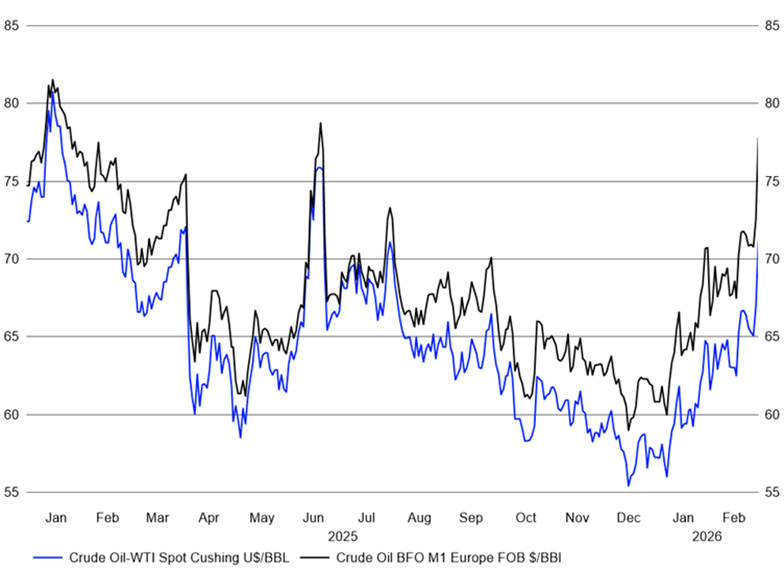

The final days of the month, however, provided a sharp reminder of how swiftly conditions can change. Large-scale US and Israeli strikes on Iran, and subsequent retaliatory missile and drone attacks across Israel and several Gulf states, raised the risk of a broader regional conflict and, crucially, disruption in the Strait of Hormuz. Oil prices jumped sharply, with Brent briefly trading at and above US$80 per barrel – a level not seen in over a year – as shipping was disrupted and insurers withdrew cover for some vessels, prompting ships to avoid the area.

Oil Price in US Dollars

Source: LSEG Workspace.

The market response was familiar for an energy-driven geopolitical shock. Equities weakened, especially in energy intensive and trade sensitive sectors; government bonds and the US dollar firmed; and traditional safe havens such as gold, the Swiss franc and the Japanese yen rose. As March began, these dynamics contributed to a bout of risk aversion in European and Asian equity markets – a reminder that geopolitical risks can quickly interrupt progress.

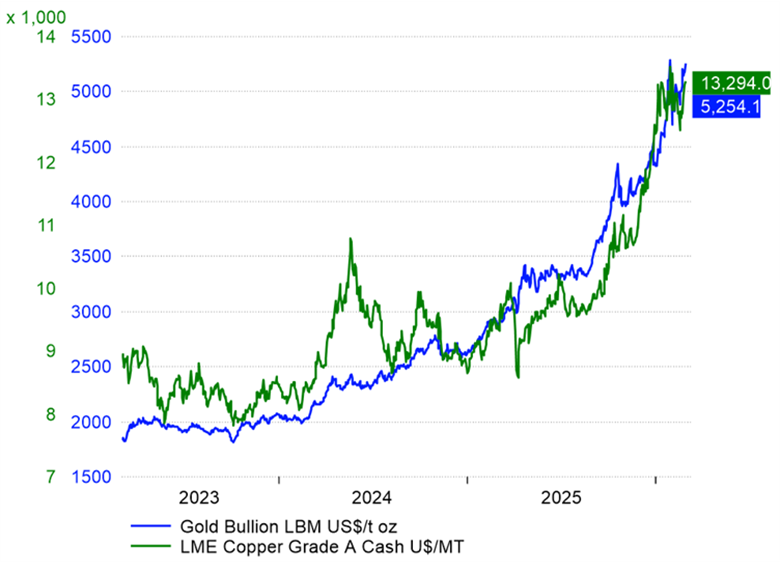

Gold and Copper Prices

Source: LSEG Workspace.

From a portfolio standpoint, this episode reinforces the role of real assets and diversifiers within a multi asset framework. The T. Bailey funds maintain strategic exposure to commodities, including gold and copper, and to a range of absolute return strategies designed to help offset equity and duration risk in periods when shocks are driven as much by geopolitics as by economics.

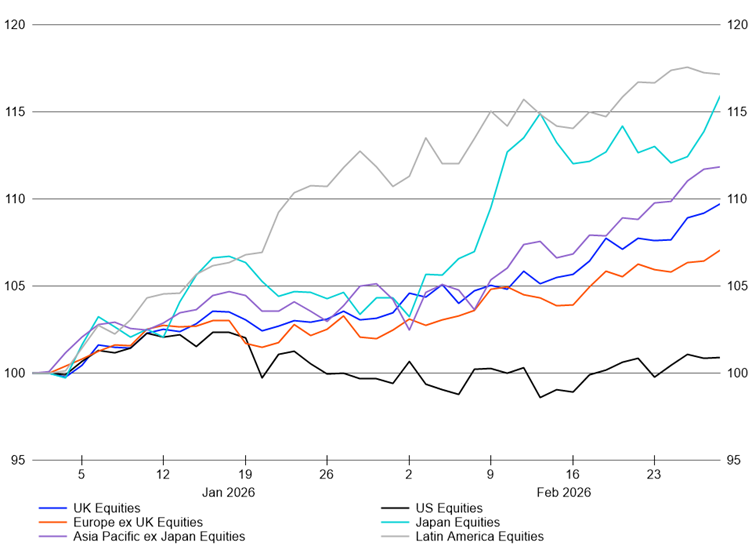

One of the most notable features of the opening months of 2026 has been the outperformance of Asia and emerging market equities up to the end of February. Japan continues to benefit from a rare combination of decisive political leadership under Prime Minister Sanae Takaichi, ongoing corporate governance reforms, and an environment of gradually rising wages and inflation that marks a meaningful break from decades of deflationary stagnation.

More broadly, emerging markets have extended the powerful rally that gathered pace in 2025, supported by relatively stronger fiscal positions, better anchored inflation and a weaker US dollar, with Asia ex Japan in particular enjoying robust earnings momentum.

The T. Bailey funds entered 2026 with a deliberate tilt towards Asia and emerging markets via specialist active managers with genuine regional expertise such as JK, Zennor, Merlin Fidelis and Baillie Gifford. This reflects our conviction that global growth and capital flows are becoming more multipolar. Opportunities are no longer confined to a narrow set of US companies, and portfolios that have not adjusted to this reality are, in our view, carrying a form of concentration risk that is rarely compensated adequately.

Regional Equities: Year to date performance

Source: LSEG Datastream. Rebased to 100 at 31 December 2025. Total return in GBP terms.

The sharp early‑March sell‑off in Asian equities, triggered by concern over a potential energy shock, higher volatility in technology supply chains and a general de‑risking of crowded positions, does not invalidate that structural case. However, it does underline that even fundamentally attractive regions can experience abrupt reversals. In our view, these episodes are an inherent part of investing and are precisely why position sizing, manager selection and overall portfolio diversification matter as much as regional conviction.

At the same time, we remain mindful of evolving trade dynamics, including renewed tariff brinkmanship from the US administration and its implications for export orientated economies. These risks reinforce the case for diversified regional exposure rather than concentrated single country bets.

Key elements of the current positioning include:

- Broad regional diversification: Lower reliance on US equities than many global peers, with meaningful allocations to the UK, Japan, Asia and emerging markets, where leadership is less concentrated and valuations generally more appealing.

- Thematic balance within equities: Exposure to long term growth themes such as AI, automation, healthcare, water and waste, and insurance, but with careful sizing of higher volatility, valuation sensitive positions and an emphasis on resilient, cash generative franchises.

- Multi asset resilience: A blend of short and medium dated sovereign bonds, selective credit, alternatives and commodities designed to provide multiple, distinct sources of return rather than relying on a single hedge to perform in every environment.

Volatility will remain a feature of markets this year, and the heavy early March correction in Asian equities following the Gulf escalation is an early example of how quickly sentiment can reverse, even in markets that have led year to date. Our objective is not to eliminate such risks from the T. Bailey portfolios, but to ensure they are diversified, proportionate and consistent with the funds’ long-term objectives, and that no single story, however compelling, dominates outcomes.