The opening month of the year has been dominated by news from the US that has set the tone for global financial markets. Robust US macro data at the start of the month showed continued strong US jobs growth, accompanied by a decline in the unemployment rate and solid growth in earnings.

However, this has been a case of good news for the economy not necessarily being good news for financial markets. Concerns that continued US economic strength could lead to further inflationary pressures initially drove longer-term bond yields higher at the start of the month and have reduced expectations of further US Federal Reserve rate cuts. This applied pressure to bond markets and currencies globally. The UK gilt market faced particular scrutiny, especially in the wake of the Autumn Budget which drew attention to increased public spending plans that would necessitate additional government borrowing and corporate sector tax increases. Recent UK corporate trading updates have highlighted the negative implications for costs and hiring intentions. The UK’s fiscal position however is not greatly dissimilar to those of other major economies.

Fortunately, bond markets stabilised later in the month which also helped lift share prices. Healthcare and financial sectors started to take the lead from the technology and consumer sectors that have been dominant in recent months. It’s also worth noting that the narrative of US economic strength contrasting with challenges elsewhere in the world is not as straightforward as it might appear for equity investors. A significant 41% of S&P 500 revenues are derived from international markets, underscoring the interconnectedness of the global economy. Global economic difficulties would provide a challenge to the highly valued earnings of US companies.

Source: Apollo, 12 January 2025.

Commodities have been one of the strongest performing areas in the T. Bailey portfolios recently, with gold (accessed through the iShares Physical Gold ETC) held in the multi-asset funds, and copper, (WisdomTree Copper ETC) held in all three fund of funds’ portfolios, performing well. Whilst recent policy announcements within China to stimulate economic growth have been supportive for the price of copper, we are mindful to keep watch of its position size in the T. Bailey portfolios, particularly

given risks around US tariffs.

Source: FE Analytics. Total returns, GBP terms.

On that note, President Trump’s inauguration on January 20th brought a flurry of actions following up on his campaign promises. Financial markets have embraced a narrative of US exceptionalism, driving the US dollar to potentially overvalued levels.

Source: Daily Shot, 20 January 2024.

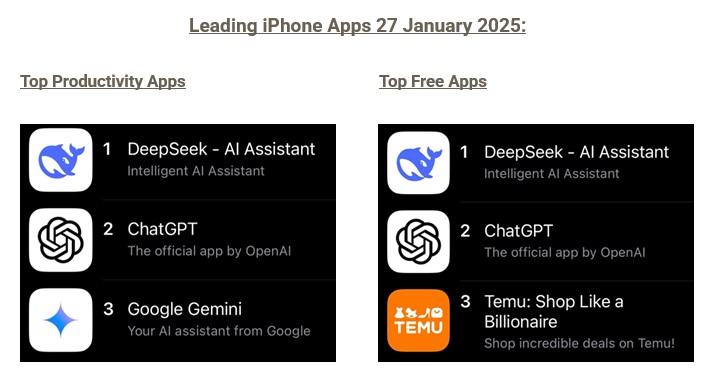

Part of that exceptionalism narrative was challenged this month with the emergence of a Chinese competitor to the US’s AI dominance. The development of DeepSeek, a cost-effective AI solution using open-source technology and less advanced hardware, has raised questions of the substantial investment made by the established tech giants in this field like Google, Meta, OpenAI and Anthropic. DeepSeek has quickly become a sought after mobile app and, more fundamentally for investors, raises challenging questions of the prevailing AI investment case. That this two-year-old start-up has the potential to disrupt established companies calls into question the necessity of the significant capital expenditure deployed to date and that is planned for the coming years. This will, no doubt, be a hot topic for the leading technology companies to address in the upcoming earnings

season.

Source: App Store, Apple (UK).

As we head into February, President Trump has already announced and subsequently postponed broad tariffs of 25% on imports from Canada and Mexico. However, for now a further 10% of tariffs on China remain and have sparked a retaliatory response. It is clear President Trump is keen on using the US’s economic momentum over other countries to his advantage to yield concessions and show action on his campaign trail promises. In the shorter term, this is a source of equity market volatility and points to the need for broad diversification across geographies and types of assets. Whether, longer-term, the US is viewed as a less reliable home for capital remains to be seen.

Markets

Equities

Relative to mainstream global equity indices, the T. Bailey portfolios maintain a bias to the unloved UK equity market where the risk-reward profile is more favourable as a result of lower valuations. Furthermore, the UK appears to be less in the crosshairs for US tariffs compared to other countries.

The iShares S&P 500 Equal Weight ETF, added to the fund of funds’ portfolios in Q4 2024, was a strong regional performer in the T. Bailey portfolios this month, having gained 5% in Sterling terms. We maintain the view that earnings growth, and as a consequence equity market performance, should broaden from here to the relative benefit of this holding.

However, the strongest performing fund this month across the T. Bailey portfolios was the First Trust Nasdaq Cybersecurity ETF. We weigh the pace of growth in this area against the somewhat lofty valuations of this ETF’s underlying companies. In contrast to larger US tech names, the sector has benefitted from the DeepSeek news as increased AI adoption raises greater security concerns and needs for solutions.

Bonds

Despite tempered expectations of further US rate cuts and the risk of higher longer-term rates, core government bonds achieved a positive return over the month. The UK Treasury Gilt (October 2018) and the iShares $ Treasury Bond 7-10 Year UCITS ETF held in the T. Bailey Multi-Asset funds were both marginally positive for January. In credit, where spreads are low by historic standards, we continue to favour a highly active approach that focuses on the debt of individual names through the Man High Yield Opportunities Fund which continues to deliver solid returns.

Commodities

Gold and Copper were both strong performers over this month. The iShares Physical Gold ETC returned 8.5% and the WisdomTree Copper ETC gained 6.6% in Sterling terms. We favour the supply and demand dynamics for both of these metals. Gold provides a hedge against geopolitical and stagflation risks whilst Copper is a beneficiary of electrification, cleaner energy and meeting the power needs for increased AI adoption.

Diversifiers

We look to alternative strategies to cushion the portfolios in periods of higher volatility. This month we increased the allocation of the T. Bailey Multi-Asset funds in this area through the introduction of a diversified absolute return fund (see below) that, with the ability to take short positions and compare the relative merits of different sectors and regions, can benefit from a fracturing world.

Your Money

This month we introduced a position in the TM Fulcrum Diversified Core Absolute Return Fund to the T. Bailey Multi-Asset Funds. This absolute return fund aims to achieve long-term returns of inflation +3% to 5% over five-year periods, with low correlation to equity and bond markets, through three broad strategies:

- Dynamic Asset Allocation: Representing around 40% of its portfolio this includes investments in stocks, bonds, and commodities, adjusting based on market conditions and trends.

- Discretionary Macro: Approximately half of this fund’s portfolio is allocated to directional and relative value trades across major asset markets that avoid correlation with traditional asset classes.

- Diversifying Strategies: The remaining 10% is allocated to short-term, trend-following strategies.

This takes the proportion of the T. Bailey Multi-Asset Dynamic Fund held in absolute return strategies to almost 17% and similarly to a little over 14% for the T. Bailey Multi-Asset Growth Fund.

This month, we exited our holding in the Schroder Sustainable Food and Water Fund across the T. Bailey fund of funds’ portfolios, in favour of the more distinctive and focused approach of the Regnan Sustainable Water and Waste Fund. This thematic fund is supported by robust structural growth drivers, such as increasing populations, urbanisation, climate change, and stricter environmental regulations. Additionally, the nature of water and waste value chains often involves companies serving local communities with minimal competition, providing defensive growth characteristics and consistent cash flows. As political trends indicate a more fragmented global economy with heightened regional competition and a shift towards local production, this theme is likely to expand.