Global Resilience Through Diversified Portfolios

Institutional frameworks under pressure: Political pressure on the US Federal Reserve and the use of tariffs as strategic leverage against allies challenged long-standing policy frameworks, prompting markets to demand a higher risk premium on US assets.

Asian and emerging market ascendancy: Japan and emerging markets delivered standout returns, supported by credible macro economic policy, strong earnings momentum and a weaker US dollar, in contrast to mounting fiscal and political strain across developed markets.

Precious metals volatility: Gold and silver surged on safe-haven demand before suffering sharp reversals, underscoring both the sensitivity of leveraged positioning and the ongoing role of precious metals as portfolio diversifiers.

Portfolio resilience: The T. Bailey Multi-Asset and Global Thematic funds generated positive returns amid episodes of elevated volatility, reflecting the benefits of broad geographic, thematic and asset-class diversification.

January was shaped less by economic data and more by events that challenged the institutional foundations underpinning asset allocation. The US Department of Justice’s criminal investigation into Federal Reserve Chair Jerome Powell – relating to congressional testimony on the central bank’s headquarters renovation – prompted Powell to warn publicly of “political pressure or intimidation” aimed at influencing monetary policy. Three former Federal Reserve Chairs and a number of global central bank governors responded with coordinated statements defending central bank independence.

At the same time, the US administration threatened escalating tariffs – rising from 10% in February to 25% by June – on eight NATO allies, explicitly linked to demands regarding Greenland’s future status. The European Union openly discussed activating its Anti-Coercion Instrument regulation, while France warned that Europe would not “passively accept the law of the strongest”.

These were by no means conventional trade disputes, but deliberate use of economic tools to pursue strategic geo-political objectives. With frameworks that markets have assumed to be structural beginning to appear conditional on political progress, investors have started to reassess their reliability and to demand higher compensation for uncertainty.

The market response was to push the price of gold on further, beyond US$5,000 per ounce and the US dollar to a four-month low as currency markets repriced risk, and equity leadership rotated decisively away from US mega-cap technology towards Asia and emerging markets.

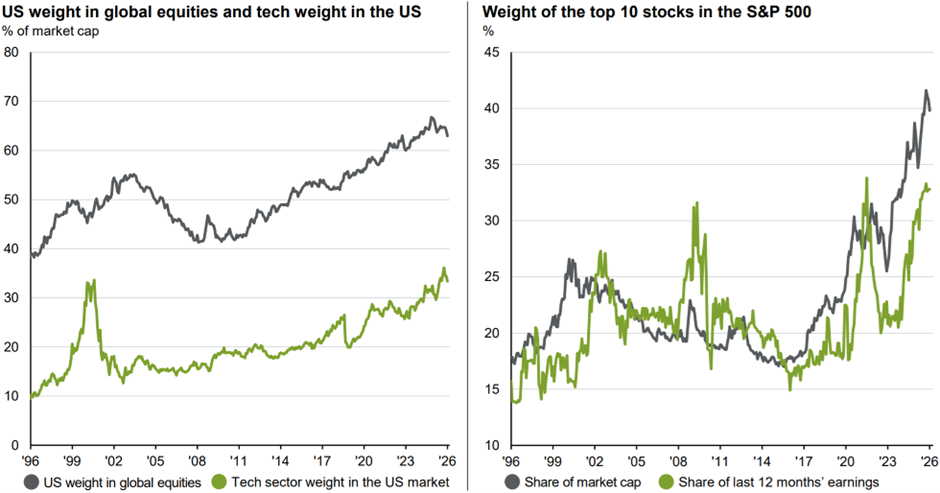

For UK investors, many of whom remain structurally anchored to US assets, weakening of institutional certainty – long a cornerstone of American financial dominance – has material implications for portfolio construction. In this context, concentration risk transitions from being a feature of “US exceptionalism” to an identifiable portfolio weakness to address.

US Concentration Risk

Source: JP Morgan Guide to the Markets – UK, Data as of 30 January 2026. (Left) LSEG Datastream, MSCI, S&P Global, J.P. Morgan Asset Management. The S&P 500 is used to represent the US market, and the MSCI All Country World Index is used to represent global equities. (Right) FactSet, S&P Global, J.P. Morgan Asset Management. The top 10 stocks are based on the 10 largest index constituents at the start of each month. Past performance is not a reliable indicator of current and future results.

The Case for Asia and Emerging Markets

Japanese equities delivered one of their strongest January starts since 1990. In the T. Bailey funds of funds this was led by the JK Japan Fund which returned 6.8% in sterling terms, supported by Prime Minister Sanae Takaichi’s fiscal stimulus package, ongoing corporate governance reforms driving share buybacks, and yen weakness enhancing export competitiveness.

Emerging markets delivered even stronger returns over the month. The Merlin Fidelis Emerging Markets Fund held across all three T. Bailey funds of funds gained 9.8%, while the Baillie Gifford Pacific Fund held in the T. Bailey Global Thematic Equity Fund rose 11.7% in sterling terms. Broad emerging market indices advanced approximately 6.7% in January alone (in sterling terms), building on gains of around 24.4% in 2025.

We believe this strength reflects fundamental improvements rather than short-lived sentiment. US dollar weakness reduces corporate financing costs, supports domestic purchasing power and eases external funding conditions for the region. Crucially, many emerging economies now exhibit stronger balance sheets, lower deficits and better-anchored inflation than their developed market counterparts, reflecting a period of comparatively disciplined monetary policy.

The contrast is clear. The IMF forecasts growth of around 1.8% for advanced economies in 2026 versus about 4.2% for emerging market and developing economies. Asia and the Pacific region alone is expected to contribute approximately 60% of global growth, and consensus forecasts point to earnings growth of around 20% for Asia Pacific ex-Japan equities in 2026, reversing years in which earnings expectations acted as a headwind rather than a tailwind.

Emerging Market Earnings Per Share Expectations

Source: Hamilton Lane, Goldman Sachs, FactSet, I/B/E/S, MSCI.

The T. Bailey funds maintain meaningful allocations to Asia and emerging markets through specialist active managers. This positioning reflects conviction in a multipolar investment landscape – one in which credible institutions, sustainable policy settings and robust growth prospects are increasingly distributed rather than concentrated.

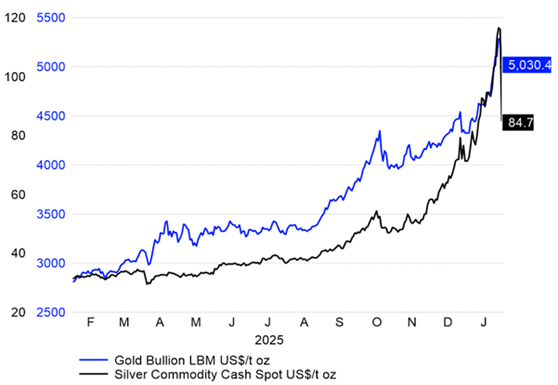

Precious Metals: Rally, Reversal and Rationale

Gold briefly surged above US$5,000 per ounce in the last week of January as investors sought safe-haven assets amid geopolitical tensions and concerns over central bank independence. Similarly, silver climbed past US$100 per ounce for the first time before briefly approaching US$120.

Repricing of institutional risk through precious metals

Source: LSEG Workspace.

However, on 30 January, both metals experienced their sharpest single-day declines in decades. Gold fell approximately 10%, while silver dropped between 25% and 30%. The nomination of Kevin Warsh as the next Federal Reserve Chair – perceived as more hawkish than incumbent chair Jerome Powell – appeared to trigger profit-taking, while earlier changes to CME margin requirements amplified the move by forcing leveraged investors to reduce positions as prices fell.

Despite the volatility, the iShares Physical Gold ETC held in the T. Bailey Multi-Asset Funds returned 13.5% in sterling terms over January. Trimming gold exposure to approximately 5.5% in both multi-asset funds as the rally showed signs of exhaustion proved prudent.

Nonetheless, the strategic rationale for holding gold within the portfolios remains intact. Central banks continue to accumulate gold at historically elevated rates, exceeding 800 tonnes annually, as part of ongoing diversification away from US dollar reserves. Elevated government debt, wide fiscal deficits, rising term premia and the growing influence of fiscal policy over monetary settings provide a supportive backdrop for gold as both a currency debasement hedge and a geopolitical risk diversifier.

Performance Across Asset Classes

Equities:

Regional and thematic diversification proved important. The JK Japan Fund (+6.8%), Merlin Fidelis Emerging Markets Fund (+9.8%) and Baillie Gifford Pacific Fund (+11.7%) materially outperformed. By contrast, the First Trust Nasdaq Cybersecurity ETF declined 7.0%, Polar Capital Insurance fell 2.8%, and Chrysalis Investments struggled as investors rotated away from high-valuation growth exposures.

UK equities provided relative stability, supported by attractive valuations and dividend yields compared with other developed markets facing similar structural headwinds. We consider the long-term risk-reward profile compelling.

Alternatives:

AQR Adaptive Equity Market Neutral detracted, falling 5.5% as correlations shifted abruptly. The other absolute return strategies held in the T. Bailey Multi-Asset portfolios delivered positive returns, providing ballast during equity volatility and reinforcing the importance of diversified, uncorrelated return streams.

Bonds:

Short and medium-dated sovereign bonds and selective high-yield exposures provided stability and income. Longer-dated yields remained under pressure as investors demanded greater compensation for institutional and fiscal uncertainty.

Commodities:

Copper continued to benefit from supply constraints, depleted inventories and optimism surrounding AI infrastructure, energy transition and urbanisation. Exposure to these structural themes remains attractive in an environment of macroeconomic volatility and geopolitical fragmentation.

Portfolio Positioning and Outlook

Current positioning reflects several structural considerations:

- Selective US exposure: focused on balance-sheet strength and durable cash flows while avoiding excessive mega-cap concentration.

- Geographic and thematic diversification: particularly across Asia and emerging markets with supportive policy settings and credible institutions.

- Real assets and commodities: including gold and copper, to provide diversification during periods of equity and bond stress.

- Absolute return strategies: offering multiple uncorrelated sources of return.

- Flexible bond exposure: emphasising shorter duration and active credit selection to limit term-premium risk.

January’s events reinforced the current positioning of the T. Bailey funds. Geographic diversification, reduced reliance on mega-cap leadership and exposure to resilient, well-governed economies – the forces that shaped January are unlikely to dissipate quickly. In this environment, a disciplined, diversified and valuation-aware approach focused on resilience and multiple sources of return, remains, in our view, the most effective way to protect and compound capital over the long term.