Key Market Insights

- Market volatility returned in November, with corrections in crowded AI and technology names reinforcing the importance of balanced, multi-theme equity exposure.

- Diversification continued to prove its value, as shorter-duration bonds, alternatives and commodities helped stabilise returns when both equities and traditional bonds came under pressure.

- The UK Budget steadied its financial markets but left structural challenges unresolved.

November was a largely flat month overall for investors following a long stretch of gains earlier in the year. It was not without volatility however as a combination of the resolution to a record US government shutdown, delayed economic releases and a sharp correction in technology related shares exposed crowded areas of the market, particularly in AI‑linked names. Equities lost momentum, technology and AI‑linked shares saw sharp moves in both directions and government bonds and other diversifiers started to earn their place in portfolios again. The construction of the T. Bailey funds of funds has this in mind: not to seek to eliminate volatility, but to temper it within a range commensurate with longer-term return objectives and to ensure that no single investment story – however enticing in the short term – dominates the performance outcome.

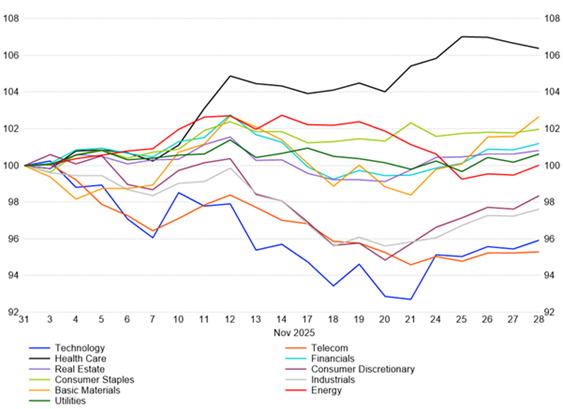

In equity markets, while AI remained the centre of attention, focus has been shifting from excitement over its growth potential to concerns over how it is funded and how sustainable that is. OpenAI, the creator of ChatGPT and a name synonymous with the theme, has spoken on sizeable infrastructure agreements over the coming years that add up to well over US$1 trillion with Oracle, Broadcom, Nvidia, AMD and Amazon. Such numbers underline how capital‑intensive AI has become. They also explain why investors are asking harder questions about who will ultimately earn an acceptable return on all this spending, and who’s balance sheets are carrying the risk. In the T. Bailey funds of funds, this environment reinforces our approach of maintaining exposure to the AI theme mainly via a specialist manager and sizing the exposure sensibly within a broader set of other themes and regional exposures – avoiding any one technology cycle dictating the overall risk profile.

That discipline showed its value as technology and AI‑exposed stocks corrected through much of the month. High‑profile short positions in the market in names such as Palantir and Nvidia, together with concerns about stretched valuations, triggered meaningful falls in the Nasdaq and other growth‑heavy indices. At the same time, more income‑generating and less cyclical parts of the market – including healthcare, insurance and quality dividend‑paying companies – held up relatively well.

Global equity sector performance in November 2025

Source: LSEG Workspace.

November also underlined the role of resilient, low‑correlation fund holdings within the funds’ equity allocations. The Regnan Sustainable Water & Waste Fund is one example: it invests in regulated water utilities and scale solid‑waste operators, whose revenues are tied to essential services and long‑term contracts rather than discretionary spending or advertising cycles. Such utilities are, by design, natural local monopolies overseen by regulators to ensure fair pricing and service quality but are also supported by a secular backdrop: governments and lenders are stepping up finance for water security just as climate volatility, ageing assets and leakage force investment. Technology also plays a part as firms digitise networks to cut losses, reduce downtime and lower energy use.

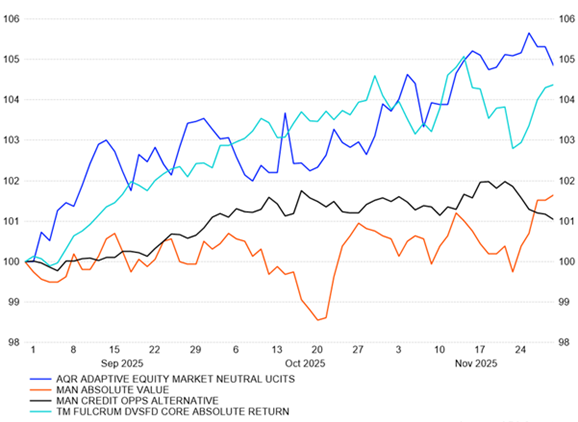

Outside of equities, November also highlighted the value of allocating to a range of diversifying assets that do not all rely on the same economic outcome. In the T. Bailey multi‑asset funds, short to medium‑dated sovereign bonds and selected high‑yield debt provide some ballast and income, but they are not the only – or even the primary – source of diversification. Absolute return funds and commodities such as copper and gold also diversify, responding differently to shifting expectations on growth, inflation and interest rates, at times when both equities and traditional bonds face headwinds. In practice, that has meant the T. Bailey funds have not had to rely on a single “hedge” working perfectly; instead, a combination of shorter‑duration bonds, alternatives, commodities and income‑oriented equities helped to smooth overall returns.

T. Bailey Multi-Asset Funds’ Absolute Return Fund Holdings – 3 Month Performance

Source: LSEG Workspace.

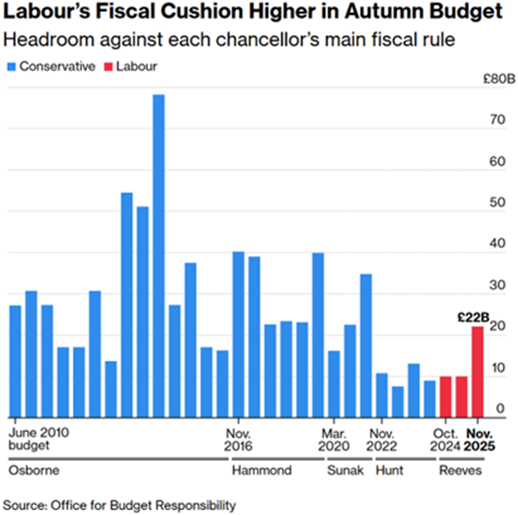

Closer to home, speculation around the UK Budget – and the reaction to it – dominated much of the news through the month. At heart, this was a tax‑and‑spend Budget designed to steady the UK’s finances and reassure gilt investors by creating a modest cushion of fiscal headroom. That has helped to pull gilt yields marginally lower and ease immediate borrowing pressures. Yet it leaves the UK’s deeper structural problems largely untouched. The result is an economy still locked into a low‑growth rut, ill‑equipped to fund rising demands on public services, particularly from an ageing population. For all the rhetoric about being forward‑looking, the package does little to shift the underlying pattern of stagnation.

Fiscal headroom against each chancellor’s main fiscal rule

Source: Bloomberg.

A defining feature of the Budget was its “buy now, pay later” approach. Many of the biggest tax‑raising measures are pushed into the later years of its forecast period, creating short‑term breathing space while shifting much of the real pain into the future. If growth were to pick up strongly, some of these measures might never fully bite; if it does not, the squeeze will land just as the government’s current mandate is drawing to a close. That may be enough to keep the Labour party broadly united for now, but the public mood is likely to be less forgiving. With local elections on the horizon, voters may well use the ballot box to register frustration at a settlement that offers little visible benefit today and depends heavily on hope about tomorrow. Political volatility therefore looks set to continue, even if the Budget has calmed markets for the moment.

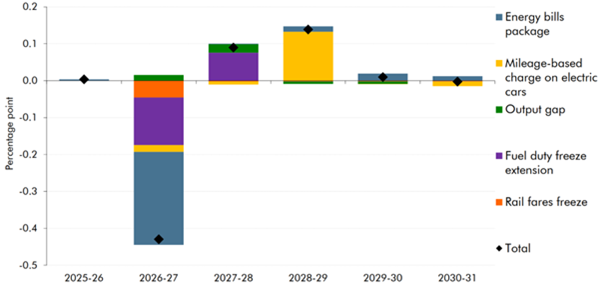

From an economic standpoint, back‑loading tax rises has one clear advantage: it helps to keep near‑term inflation pressures in check and gives the Bank of England more room to further cut interest rates. That shift will be welcomed by households facing higher mortgage costs and by businesses looking to invest. Beyond this cyclical relief, however, there was disappointingly little in the Budget to actively lift the UK’s growth potential. Industrial strategy was fragmented, and incentives for productivity, investment, and innovation were inconsistent.

Impact of Budget policies on CPI inflation

Source: Office for Budget Responsibility, 26 November 2025.

A more stable gilt market and the prospect of lower interest rates support asset prices, including UK shares, by easing financing conditions and lowering discount rates. But the lack of a convincing growth story continues to weigh on the outlook for domestically focused companies that depend on UK demand. Even so, UK equities as a whole still offer relatively low valuations and attractive dividend yields compared with many other developed markets facing similar or worse structural challenges. For long‑term investors, that combination of income and value keeps the UK market of interest.

Taken together, November’s moves reinforced several principles that guide the T. Bailey funds of funds. First, returns should come from multiple sources – regional, sectoral and stylistic – rather than reliance on a narrow cohort of winners. Second, fixed income and alternative diversifiers remain integral to meeting risk and return targets, especially now that bond yields offer more credible income. Third, valuation discipline and position sizing are central: thematic and higher‑volatility exposures are held, but within limits that reflect their risk profile and correlation characteristics. For investors, the result is a set of portfolios designed not to chase every short‑term market move, but to combine growth, income and resilience in a way that can cope with months like November.