Developed economies’ central banks have remained centre stage in October, with investors mulling how much they will tighten monetary policy.

Trick or Treat?

If the beginning of October was tricky, then the end was more of a treat as risk assets rebounded. I’ll include gilts under that classification as relative political stability and the expectation of fiscal responsibility returned in the UK. The edge was taken off those positive returns for sterling-based global investors by the UK currency’s Sunak-related bounce back amidst a weakening US dollar.

Elsewhere, developed markets responded to a softening of central bank rhetoric on the amount of monetary tightness required to slow economies and inflation. The Bank of England’s Deputy Governor, Ben Broadbent, pursued a similar dialogue.

The trick at the end of the month came from China where the 20th National Congress of the Chinese Communist Party saw President Xi tighten his control which sent Chinese equities into a tailspin.

Supply vs Demand vs Pivot

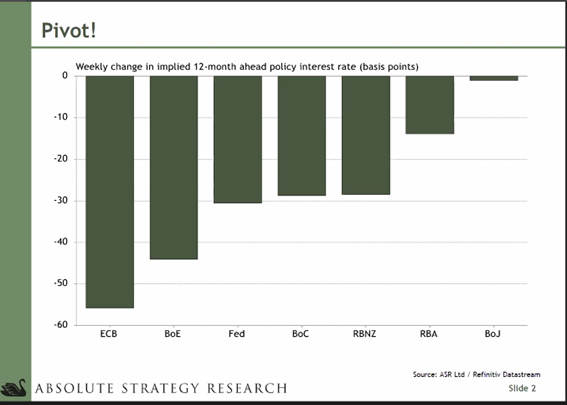

Developed economies’ central banks have remained centre stage in October, with investors mulling how much they will tighten monetary policy. The softening of language manifested itself in a lowering of expectations of policy rates over the next twelve months, as seen below:

Source: Absolute Strategy Research

Central banks are struggling with supply issues they have little influence over such as food and energy prices. Their attempts to raise interest rates to control excess demand magnified by tight labour markets risks recession, increased unemployment, and may take the froth off the housing market.

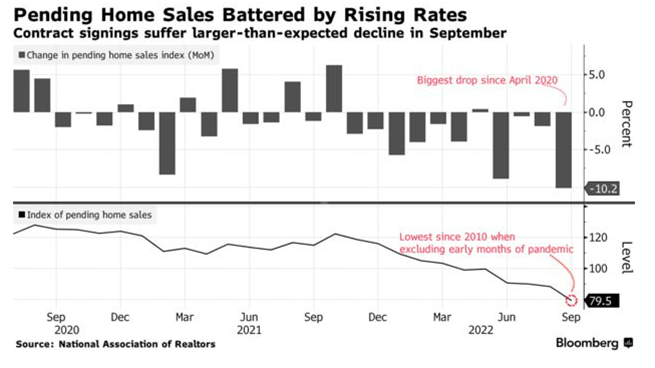

House prices fell the most since the start of the pandemic in October in the UK according to Nationwide, which isn’t a complete surprise given the recent political upheaval here. But in the US, the housing market is also reeling from mortgage rates which are close to 7% as the following chart sourced from Bloomberg demonstrates:

Pausing for Breath?

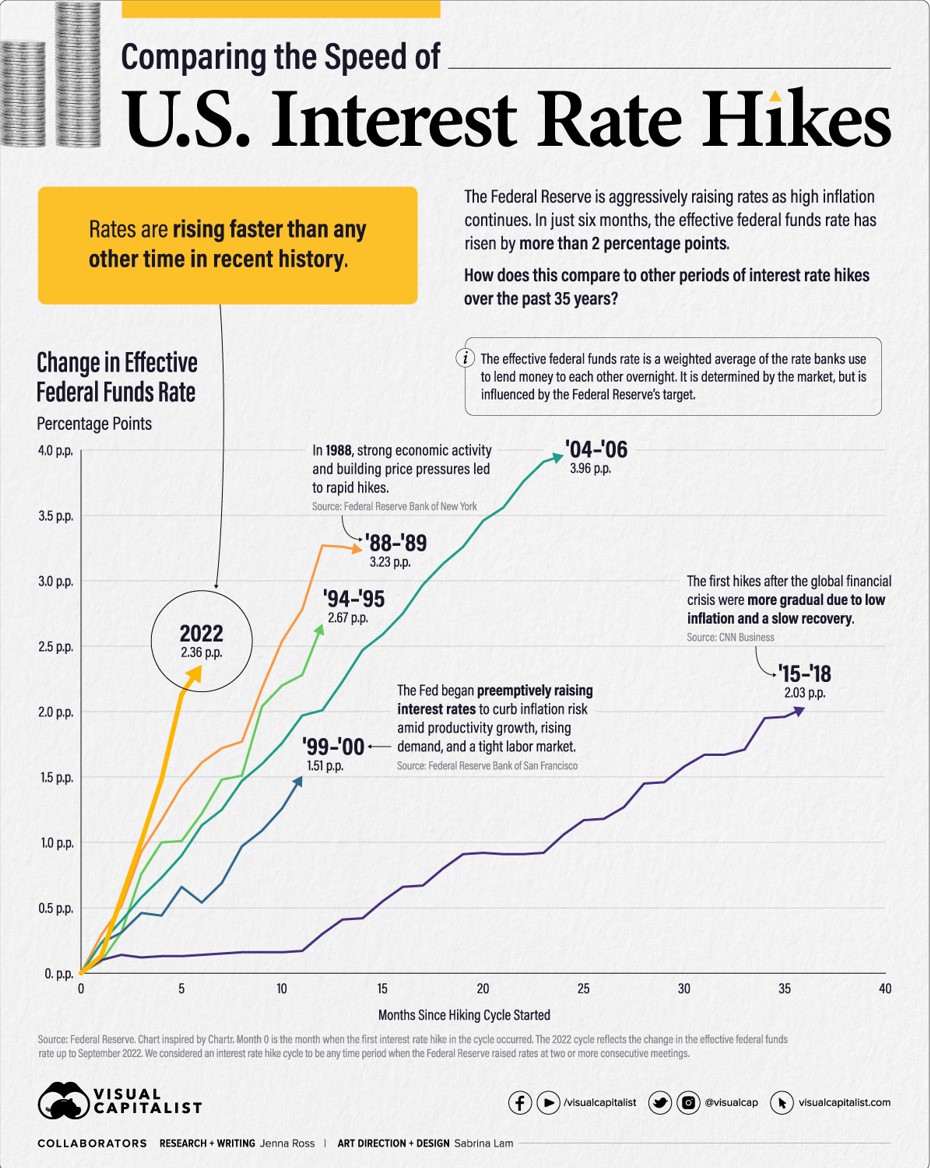

The fast pace of official rate increases risks not having the time to measure their impact given the time lag between raising rates and seeing their economic influence, is at least six months. Part of that is due to developed market central banks playing catch up after being overly loose for too long in 2021. The scramble to raise rates has been a reaction to far higher inflation rates than had been envisaged at the end of 2021.

The following chart gives context to the pace of rate increases versus history:

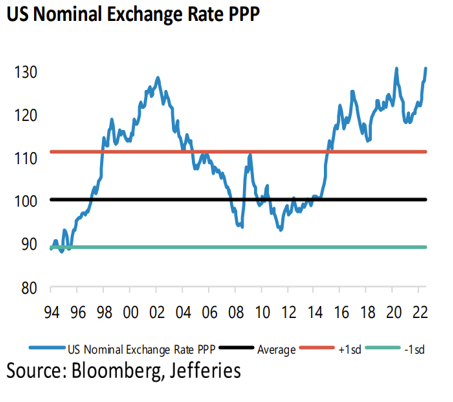

Prior to month-end weakening, the US dollar had become stretched/expensive. The above chart shows the US currency’s Purchasing Power Parity going back almost thirty years.

Inflation Peaking?

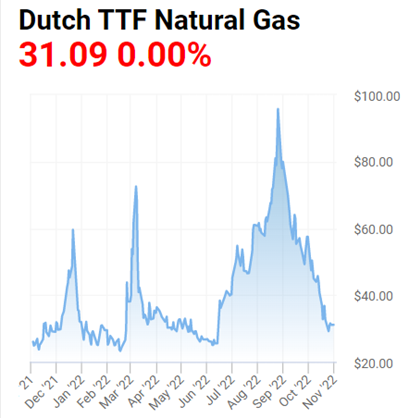

It’s too early to say and recent numbers from Europe and the UK make for sombre reading. Food inflation remains sticky throughout those areas but energy and fears over energy shortages, especially natural gas, have abated due to European countries moving to almost full storage as well as being helped by recent mild weather which is forecast to remain through November. Germany, France, the Netherlands and Italy, who between them make up two-thirds of natural gas usage, are at 95%, 98%, 93% and 93% of their maximum capacity. To understand the impact that has had on natural gas prices, it is worth looking at the price chart of the leading European natural gas contract, the Dutch TTF Natural Gas contract and its precipitous fall from the highs of late summer:

Source: OilPrice.com

Oil prices are back to where they were a year ago having been 50% higher in the spring.

Markets – A Game of Two Halves

Against this backdrop, financial market volatility has barely ebbed. Inflation numbers have yet to subside and remain firmly in focus yet the expectation is that inflation will fall in the months ahead as year-on-year comparisons become meaningful. The key influence for financial markets in October was the perception that future official interest rate increases will be less severe than embedded into futures markets. Earnings were mixed but generally not good for the big tech companies and their share prices took it on the chin. Amazon beat estimates but pointed to a gloomy holiday season.

Whether the rally in equities and bonds that took place in the second half of October is another bear market rally or reflective of some investors putting money to work remains to be seen. Thematic equities bounced well as did the share prices of European and US businesses, beyond the bigger companies for a change. Within thematic equities, interest rate sensitive themes such as infrastructure led the pack. Energy transition was another strong theme in October. While inflation is less of an issue in the far east, the region’s returns were negatively impacted by China and President’s Xi’s increasing political power.

Bond market oscillations unsurprisingly continued given the mixed macro-economic data updates illustrating both economic slowdown plus firm labour and inflation reports. The comfort for bond investors came from central bankers’ softer rhetoric on monetary policy. Credit spreads narrowed marginally over the month from recent highs.

Commodities posted negative returns across the board, reflecting the economic outlook.

The US dollar traded lower towards the end of the month but was stronger over the whole month. Sterling was the notable recovery story, reflecting a more stable political scene – for now.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok