Key Market Insights

- Global equities rose despite pronounced policy uncertainty, a US government shutdown, and technology sector volatility.

- Gold exemplified safe-haven demand, soaring above US$4,300/oz before a swift correction.

- Trade tensions briefly rattled markets, but a late-month US-China tariff truce and strong AI-led earnings helped lift risk assets.

The month opened with a US government shutdown after Congress failed to reach agreement on a budget. Roughly 750,000 federal employees were furloughed and many public services temporarily halted. Meanwhile, the IMF warned of subdued global growth and persistent inflation pressures, reinforcing expectations that monetary policy would likely remain restrictive. Conditions were more constructive in Asia: the Reserve Bank of India held rates at 5.50% and raised its GDP forecast to 6.8%, while Japan’s quarterly Tankan survey showed improving confidence among manufacturers.

Healthcare was a notable sector. Mid-month, renewed White House commentary on drug-pricing reform – including references to “most favoured nation” rules and greater scope for government-negotiated discounts – put pressure on several large pharmaceutical companies, particularly those with significant exposure to US pricing dynamics. Areas of the market focused on biotechnology and medical technology innovation fared more resiliently as investors rotated away from companies most exposed to potential regulatory change.

Gold illustrated safe-haven behaviour through much of the month. The metal surged above US$4,300 per ounce on 16 October, driven by geopolitical uncertainty, central-bank accumulation and demand for inflation hedging. In the T. Bailey Multi-Asset funds we took this strength as opportunity to take partial profits and reduce positions closer to long-term targets. The timing proved beneficial: during the week of 21 October, gold experienced one of its steepest single-day declines in years. However, in sterling terms, gold remains up more than 45% year-to-date. The Multi-Asset funds both currently hold gold positions of around 5%, providing diversification benefits without excessive concentration.

Gold Bullion Price

Source: LSEG Datastream.

Following a brief period of relative calm trade tensions intensified mid-month when US President Trump threatened a 100% tariff on Chinese imports from 1 November, prompting Beijing to tighten export restrictions on key rare-earth materials. Global equities sold off, led by technology and AI-linked stocks, and cryptocurrency markets saw large liquidations as risk appetite faded. By the following weekend, however, US Treasury Secretary Scott Bessent and China’s Vice Premier He Lifeng held talks and agreed to resume negotiations, easing immediate concerns. Late in the month, the US and China announced a one-year tariff truce, with the US rolling back selected levies and China easing restrictions on critical minerals, supporting a rally in global equities.

Central bank decisions dominated the final week of October. The Federal Reserve reduced interest rates by 25 bps to 3.75%-4.00%, responding to signs of labour market softening. The Bank of Canada cut its policy rate to 2.25% but signalled that its easing cycle was nearing completion. The European Central Bank held rates unchanged at 2.00% for a third consecutive meeting. The Bank of Japan kept its policy rate at 0.5% though two board members voted for an increase, and the yen weakened past ¥153 per US dollar. This divergence in monetary policy supports the case for maintaining geographic diversification across the T. Bailey portfolios.

September’s US inflation data, released during October despite the government shutdown, showed the US Consumer Price Index rising 0.3% monthly and 3.0% annually, slightly below consensus expectations. The data reinforced market expectations for further Federal Reserve easing and pushed Wall Street to fresh record highs. Quarterly earnings from major technology companies revealed continuing AI-related revenue growth but also raised questions about capital discipline. Meta, Amazon, Alphabet and Microsoft all reported results, but investor responses varied significantly. Nvidia reached a US$5 trillion market capitalisation, the first company to do so, after announcing strong chip sales and US$500 billion in confirmed AI hardware orders. Alphabet’s results were well received for a balanced approach to capital expenditure, whilst Meta faced selling pressure as investors questioned the sustainability of its infrastructure spending plans.

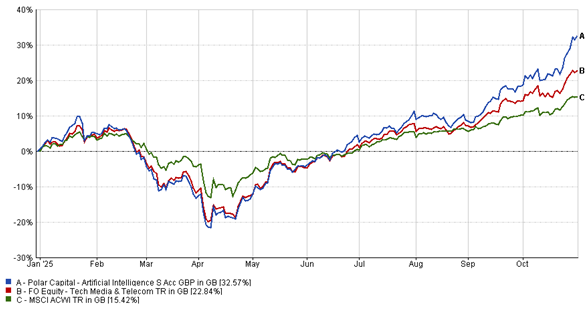

The Polar Capital Artificial Intelligence Fund, held across the T. Bailey funds of funds portfolios, achieved a 12.0% return in October. This performance was driven by positive results from Nvidia and sustained momentum in AI infrastructure investment. Additionally, the fund has been expanding its investment focus to encompass the broader AI infrastructure ecosystem, as well as entities that are beginning to realise benefits from the adoption of artificial intelligence technologies.

Polar Capital Artificial Intelligence Fund – Year to date performance

Source: FE Analytics.

Sterling weakened late in the month as UK borrowing data showed a deficit of £99.8 billion for the six months to September, above expectations and the highest September total in five years. The figures, combined with the upcoming UK Budget on 26 November and concerns over fiscal sustainability, weighed on UK assets.

Another notable data point came from Berkshire Hathaway, which reported a record cash position of around US$381.7 billion. The size of this reserve – accumulated steadily as equity indices reached new highs – serves as a reminder that valuation discipline remains important amid market optimism. The T. Bailey portfolios maintain meaningful allocations to regions and sectors trading at more attractive valuations than US large-cap growth stocks.

Looking towards November and year-end, markets face several tests. Further central bank meetings will clarify the path for interest rates across major economies. With fundamental trade and technology issues unresolved, US-China negotiations will continue throughout the one-year truce. The technology sector faces ongoing questions about whether elevated capital expenditure on AI infrastructure will translate into sustainable earnings growth. The IMF’s Global Financial Stability Report, published in late October, warned that whilst markets appear calm, underlying fragility remains elevated due to stretched valuations, high sovereign debt levels and growing exposure through non-bank financial institutions.

Throughout October, disciplined positioning, geographic diversification, thematic exposure to long-term structural growth trends and selective profit-taking were important in managing risk while maintaining exposure to potential opportunity. As markets enter the final weeks of the year, diversification, thematic conviction and valuation awareness remain central to the investment approach of the T. Bailey funds.