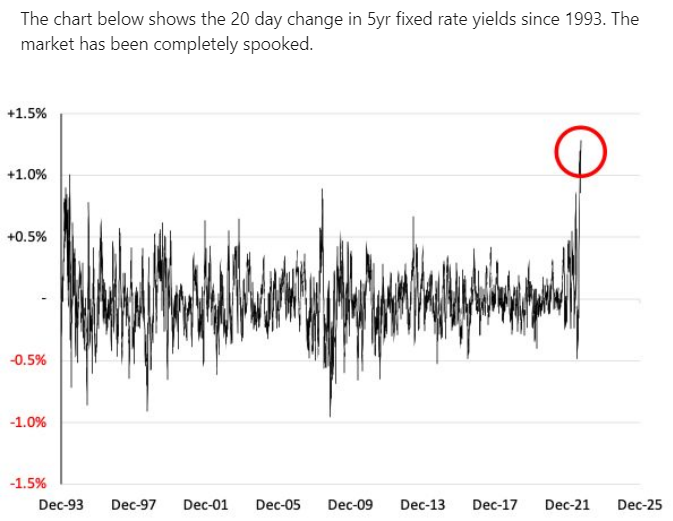

September has magnified the rollercoaster of emotions for investors as financial markets oscillated widely

Without trying to be flippant about the current situation, the following music and film references sprang to mind as a reflection of what happened towards at the end of September, especially in the UK.

Those of a certain generation may recognise the above album cover – Selling England by the Pound.

Slightly younger, Life (investing) is a Rollercoaster is both a book and song by Ronan Keating.

September has magnified the rollercoaster of emotions for investors as financial markets oscillated widely; none more so than the UK bond markets and Sterling over the final six days. Investing emotionally or throwing in the towel may provide immediate relief but rarely proves to be of benefit in the long run.

An older vintage, the film depicted below is an accurate description of the events of Friday, 23 September 2022.

The Good

A pro-business ‘mini-budget’ to follow the energy price cap announced previously.

The Bad

The decision to ignore the Office of Budget Responsibility (OBR) and go beyond the necessary by cutting the top rate of income tax to 40% from 45% (subsequently rescinded on 3 October) and not inflation-adjusting tax thresholds. Timing and execution were poor. Where was the Minister for Common Sense?

The Ugly

The market reaction (with acknowledgement to George Godber of Polar Capital).

As we know the Bank of England had to step in to prevent systematic risk to the UK bond markets. Sterling plummeted, albeit against a strong dollar, to a multi-year low.

All this happened after the first half of September was dominated in the UK by the passing of Queen Elizabeth II on 8 September followed by a period of mourning and the state funeral on 19 September.

The grieving of the nation for their departed monarch provided a collective national identity backdrop for the incoming Prime Minister, Liz Truss, after the announcement of her Conservative party leadership success on 5 September and confirmation by the Queen at Balmoral on 6 September.

Having announced an energy price cap on the morning of 8 September, the new PM and her key cabinet appointees found themselves with an extended period to get their act together while the nation mourned and the Queen’s farewell was planned.

What happened on Friday, 23 September after Chancellor Kwasi Kwarteng’s ‘mini budget’, will live as an outstanding example of a reversal of fortunes, or misjudgement of the pulse of a nation:

A look at a chart of the thirty year UK Government bond (Gilt) in September gives a snapshot of the price volatility. At one stage, the thirty year gilt had lost over 25% of its value in three days before the Bank of England stepped in and bought a few billion!

Source: FT.com

And, as we know, Sterling plummeted against most currencies but especially against a strong dollar, before recovering as the following chart shows.

Source: Tradingview.com

Globally, September will be remembered for being a month that tested investors’ resolve as persistent inflation, way above central banks’ targets, provided the back drop for a procession of official interest rate increases led by the US Federal Reserve and accompanied by the Bank of England and the European Central Bank.

Hopes for signs that inflation was peaking failed to materialise and the rhetoric from central bankers in North America, the UK and Europe was increasingly directed at stamping out inflation even if it means recession. That rhetoric was responsible for a poor month for financial assets across most asset classes.

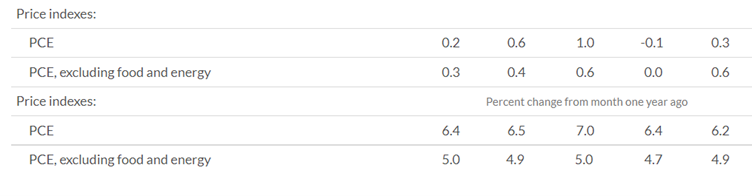

The final day of September saw the US Federal Reserve’s favoured measure of inflation released. The Personal Consumption Expenditure (PCE) came in above estimates and therefore disappointed markets and the ‘Fed’.

Source: US Bureau of Economic Analysis (BEA)

Wild Card

Ukraine has made significant progress in its fightback against Russian aggression but Putin has raised the stakes by the illegal annexation of four regions in Ukraine with a nuclear threat to defend them, claiming, illegally, that they are now part of Russia.

The reality is more akin to developing a better bargaining position to enter into a ceasefire before negotiating a face-saving conclusion to his ‘special mission’ ahead of winter. It is unlikely that Ukraine will play ball without significant pressure from western backers.

The conflict remains a wild card event for financial markets.

September by Asset Class

Currencies

The US held sway during September and despite becoming stretched and overvalued on a trade-weighted basis, the Federal Reserve’s monetary policy rhetoric for higher rates led to the US currency’s strengthening throughout the month. Sterling proved to be the laggard given its own issues, referenced earlier, at the end of the month. Other than that, it was another month of broad US Dollar strength. The following chart from TradingView.com illustrates the strength of the US Dollar on a trade-weighted basis (DXY) this year:

Source: Tradingview.com

Bonds/Debt

A continuation of bad news for bondholders. The desire of central bankers to conquer inflation by raising rates took its toll on all bond markets in September.

As they have done for most of 2022, yields rose and prices fell from government bonds to investment grade and high yield with spreads widening in the latter two categories.

Stresses re-emerged in EU government bonds with the onset of a new right-wing Italian government causing Italian yields to rise in absolute and relative terms.

The Bank of England stepped in to prevent systematic risk from pension fund selling to meet margin calls on their derivative positions structured for Liability Driven Investment (LDI) purposes.

The gyrations in the gilt market were breath-taking and caused ripples across many bond markets. Quantitative tightening (QT), where central banks are unwinding their balance sheets by selling debt built up post the pandemic, didn’t help bond markets. Indeed, the Bank of England reversed its intentions and bought debt to alleviate the aforementioned gilt market systematic risk.

Inevitably, bond markets in 2022 have recalibrated from a sustained period of being the wrong price buoyed by over-accommodative central bank monetary policy, which is now in reverse.

Equities

It was a tough month for equities globally with the prospects of higher official interest rates and a global recession weighing on all markets. The damage was indiscriminate. One or two defensive sectors managed to buck the negative returns; healthcare and insurance eking out small positive outcomes in September. There was an air of capitulation from investors that saw investor confidence plummet.

Commodities

A rollercoaster ride but one that mostly delivered positive outcomes over the month in contrast to most other asset classes. Energy (via oil and gas) prices fell and were welcome from an inflation standpoint. Agricultural prices ended firmer over the month and industrial metals, notably copper, recovered from their lows.

What Worked

Exposure to healthcare and insurance helped the T. Bailey Growth Fund and our two multi-asset funds. The latter were also aided by commodity exposures and by their allocation to absolute return funds which collectively bucked the extremes of negativity coursing through bond and equity markets.

Any non-Sterling exposures helped as Sterling suffered from a strong dollar and latterly from its well-documented travails in the last week of September. The varying degrees of foreign currency exposure prevalent in the Dynamic Fund, Multi-Asset Growth Fund and Growth Fund helps to explain why they delivered similar outcomes despite different levels of equity risk and there being no bond exposure in any fund.

It is difficult to promote having no exposure to bonds as a strategy that worked but the typical balanced or multi-asset fund will have bonds as a lower risk asset in their portfolios. The lack of value in bonds for some time has led us to avoid all forms of debt for the multi-asset funds.

What Hasn’t Worked

Our philosophy of investing in businesses within long-term investment themes with solid balance sheets, good free cashflow, and low labour intensity has underperformed this year.

Our focus on themes and financial strength in businesses typically involves exposure to small and mid-size companies. Large and mega-capitalisation businesses have led the way in 2022, especially those based in the US and UK, trouncing the returns of non-US smaller companies. We are currently seeing extremes of performance difference between the FTSE 100 and those smaller and mid-cap sectors.

We are often directed to the performance of the FTSE 100 as a ‘safe-haven’ of value investing which has done well this year. However, it is the large oil companies, miners and tobacco stocks that generated those returns and if equally-weighted, the FTSE 100 would have delivered negative returns. For us at TBAM, oil companies and tobacco are not a long-term theme as certainly the former will struggle to avoid being burdened with stranded assets.

What Next?

Value vs Growth

One of our favourite instances of inappropriate labelling. There is much pessimism priced into the valuations of companies inhabiting our preferred themes, so many financially sound ‘growth’ businesses look like excellent value at current prices. Whether they participate in a bear market rally is uncertain. It is impossible to predict what will happen over the remainder of 2022 but the valuations of businesses we like should generate appropriate outcomes into 2023 and beyond.

Secular vs Cyclical

One of the problems for North American and UK economies is the tightness of labour markets giving rise to fears of wage/price spirals. Current strike actions are evidence of this concern. US unemployment data, released the first Friday of each month for the previous month, has become a must watch indicator for markets. However, it is the housing market that usually leads the way in ascertaining if the US economy is slowing. Two successive price declines for houses would suggest slowing activity. This is perhaps unsurprising as US mortgage rates have accelerated to north of 6.5%.

It seems only recently that politicians were fielding questions over the need for universal income as unemployment was predicted to accelerate due to the greater use of robots. One could be forgiven for thinking the current employment picture is a cyclical rather than secular issue.

Swiss Watches

Sharp increases in rates, in this case bond yields, often bring leveraged exposures into the spotlight. Credit Suisse’s investment banking arm is currently under such a spotlight. Despite reassurances from its CEO, it remains a watching brief as to whether official assistance for Credit Suisse has a material impact on financial markets.

Summary

The events of 2022 have directed investors’ flows towards large cap US and UK equities. While it is impossible to predict what happens in the balance of 2022, the sell-off and built in pessimism in financially sound businesses leaves some excellent value in themes we want to own over the long-term. Sterling’s fall has effectively put up a ‘For Sale’ sign to international, especially US, buyers for quality, robust businesses.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok

Source: US Bureau of Economic Analysis (BEA)

Source: US Bureau of Economic Analysis (BEA)