The oil price has declined and underperformed other commodities over the last three years, falling from around $90 per barrel to approximately $60 today:

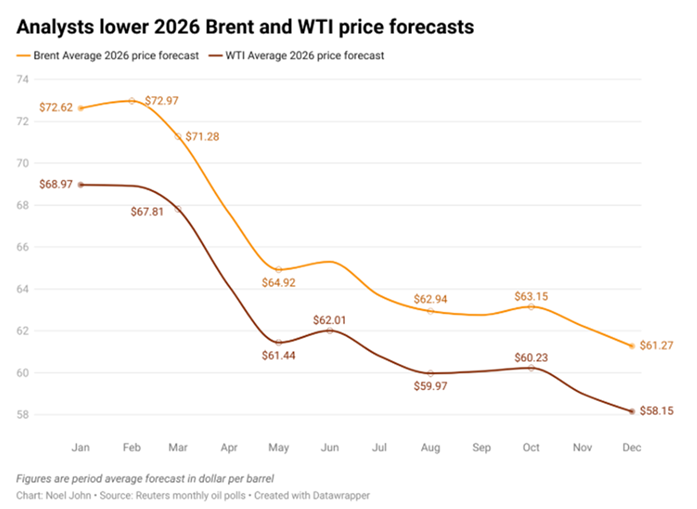

Looking ahead, oil price forecasts from bank analysts for 2026 remain conservative. The average forecast for Brent crude stands at $61.27 per barrel, with WTI forecast at $58.20. Analysts expect the oil market to move into surplus next year, by around 0.5–3.5 million barrels per day.

Forecasts within the analyst poll range from a high of $68 per barrel from DBS Bank, which factors in a potential OPEC+ production pause and possible new sanctions on Russia, to the most bearish outlook from ABN Amro and Capital Economics, both of which forecast Brent at $55 per barrel. For context, Brent crude was trading at approximately $60 as of 7 January.

The chart below illustrates how analyst forecasts for 2026 have been repeatedly revised down throughout 2025.

Brent and WTI prices declined by approximately 19% and 20% respectively during 2025, their sharpest annual falls since 2020, largely due to production increases from OPEC. Saudi Arabia alone increased production by roughly one million barrels per day over the course of the year.

According to OPEC’s most recent monthly report, global oil supply and demand are expected to be closely balanced in 2026, with both projected at approximately 106–107 million barrels per day.

On the demand side, it is worth noting that forecasters such as the International Energy Agency have softened their long-standing “peak oil demand” thesis. A slowdown in global electric vehicle adoption has contributed to expectations that oil demand will continue growing through to at least 2030.

When viewed relative to other commodities, oil appears particularly depressed. At current prices, one ounce of gold buys around 80 barrels of oil. This ratio has only been exceeded once in the past 35 years, during the brief period in 2020 when oil prices turned negative at the height of the Covid pandemic.

Given the prevailing bearish consensus, it is worth considering an alternative perspective. Goehring & Rozencwajg (G&R), a specialist natural resources investment firm, have recently argued that oil may be poised to take over the leadership baton from gold. The firm was notably constructive on gold three years ago and now sees a similar opportunity emerging in oil markets.

Their thesis highlights the extremely negative sentiment surrounding oil, reflected in the bearish price targets outlined above. G&R argue that oil is widely perceived as obsolete and structurally challenged, leading to significant under-ownership. The energy sector now accounts for approximately 4% of the S&P 500, compared with over 10% a decade ago.

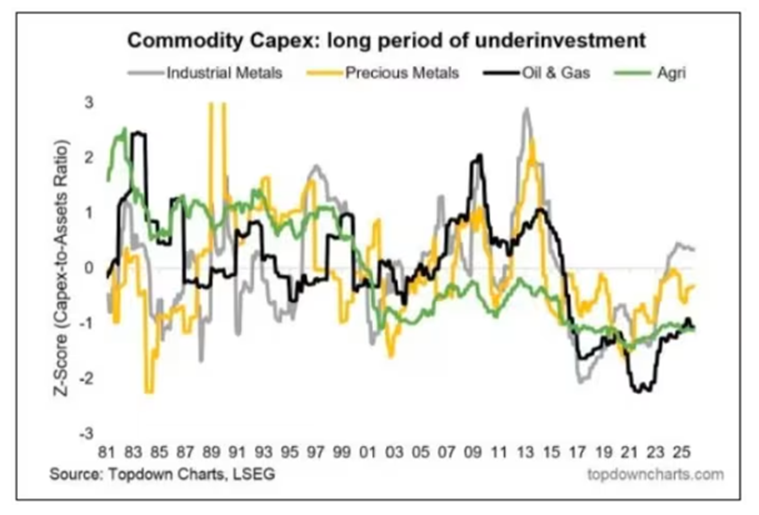

G&R contend that when investor pessimism becomes sufficiently extreme, capital investment dries up. In such an environment, supply can no longer respond adequately to demand, ultimately driving prices higher. The chart below illustrates how periods of sustained under-investment are historically unsustainable.

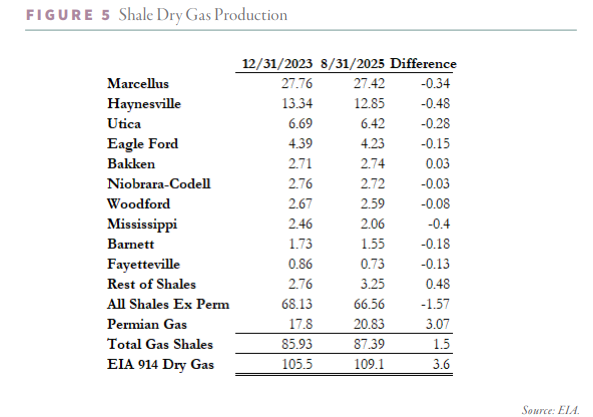

They also highlight how global energy supply dynamics have shifted over the past two decades. Growth in oil production outside of OPEC was driven almost exclusively by onshore US shale. That growth now appears to be stalling. G&R argue that US shale production is rolling over, with even the prolific Permian Basin believed to have peaked due to geological constraints.

The table below shows that since 2023, production across the major US shale basins has largely stopped growing, with the Permian Basin expected to move ex-growth.

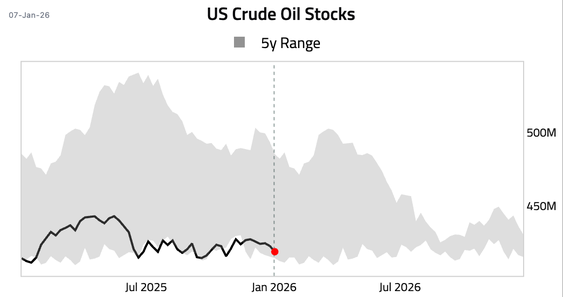

In addition, the chart below shows that current US crude oil inventories are near the lower end of their five-year range, leaving little margin for supply disruption.

Despite renewed political rhetoric, including calls for the US to “drill, baby, drill” following Donald Trump’s return to the White House, economic realities remain a constraint. At current oil prices of around $60 per barrel, US exploration and production companies are not sufficiently incentivised to invest. While many producers can cover operating costs at $50 to $60 per barrel, new drilling activity typically requires oil prices closer to $70 to $75 to generate acceptable returns.

Over the past 18 months, Saudi Arabia has acted as the swing producer, increasing output to support global supply. A key question is how much of this strategy has been influenced by US political pressure to contain inflation. Another is how sustainable this approach is at current oil prices. Saudi fiscal pressures are rising, with the government increasingly reliant on debt issuance to fund its budget.

It remains uncertain whether Saudi Arabia will maintain this stance through the US mid-term elections. The IMF estimates that the Saudi government requires an oil price of approximately $90 per barrel to balance its annual budget.

Taken together, these dynamics suggest that the oil market may be approaching an inflection point driven by the capital cycle. With the energy industry starved of investment, non-OPEC supply growth faltering, decline rates accelerating in existing oilfields, and global spare capacity shrinking, the conditions for a future re-pricing of oil may be quietly falling into place.

At T. Bailey, this type of analysis forms part of our ongoing assessment of the investment landscape, particularly in sectors where capital cycles and investor sentiment may be misaligned with longer-term fundamentals. While we remain mindful of short-term uncertainties, monitoring these developments helps ensure we are well positioned to identify opportunities as market conditions evolve.

Ben Ridley is Fund Manager at T. Bailey Asset Management.