Broadcom's earnings disappointment and rising Treasury yields triggered a sharp market reversal during the week, prompting renewed questions about the sustainability of the AI investment cycle. The update examines whether current valuations are being supported by genuine end-user demand or by a self-reinforcing capital expenditure boom that may be approaching its limits.

This week began at all-time highs and ended with the worst single day for US equities since October. Broadcom's record earnings were punished for being merely extraordinary. But the more important question is not whether the numbers were good enough - it is what they are actually made of.

On Wednesday evening, Broadcom reported exceptional results yet the stock fell over 12% on Thursday and a further 8% on Friday, because its forward guidance, particularly around AI revenues, had missed analyst expectations. That is the market this AI cycle has become: one in which a small miss on a record quarter is treated as a failure. South Korea's Kospi index - up over 100% in 2026 to the end of May as the world's most concentrated pure play on the AI buildout - fell as much as 7% during Friday’s session. A jobs report showing US hiring at more than double the expected rate compounded the move, pushing Treasury yields sharply higher and extinguishing what remained of any rate-cut narrative.

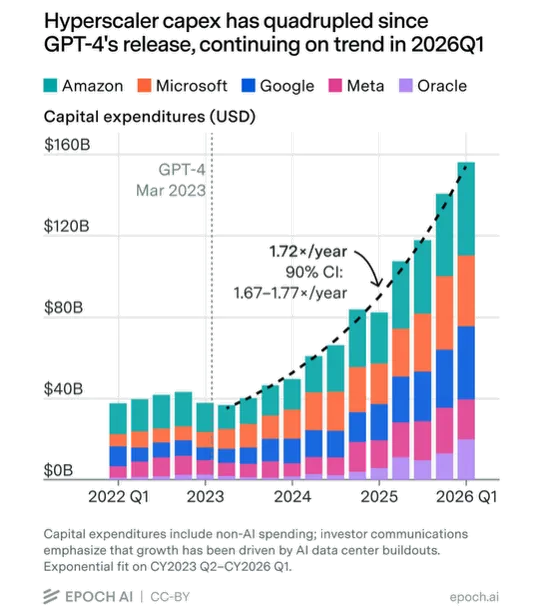

The earnings growth underpinning AI equity valuations has been generated by the capital expenditure cycle itself rather than by proven end-user demand. The hyperscalers and their suppliers have been spending - on chips, data centres, energy infrastructure - at a rate that has produced strong revenues and earnings throughout the supply chain. The capex cycle has been validating itself through the earnings of the very companies it is paying. Whilst this is not a fraudulent arrangement, it is a circular one, that will eventually assert itself.