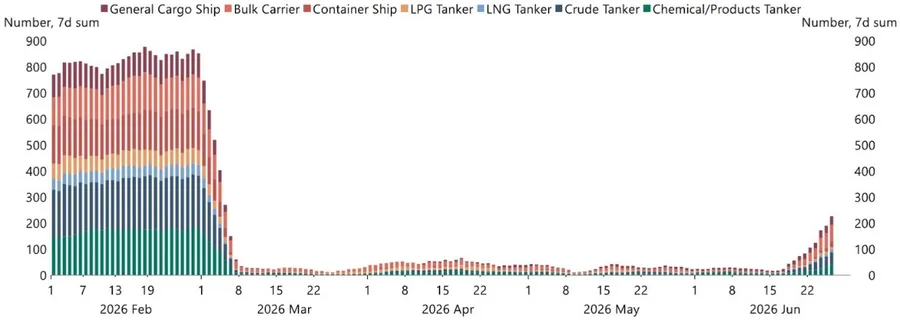

- A US-Iran deal - signed at Versailles, breached eight days later: US President Trump signed a memorandum of understanding with Iran on 17 June, earmarking US$300 billion for reconstruction and reopening the Strait of Hormuz toll-free for sixty days. Iranian drones struck two transiting vessels by 25 June and the US struck back. The agreement is in place but whether it holds into July is the prevailing question.

- A shared global energy shock for central banks: The ECB raised its deposit rate to 2.25%, its first hike in nearly three years. The Bank of Japan lifted rates to 1.0%, the highest since 1995. Kevin Warsh's first FOMC meeting held at 3.5% to 3.75%, but nine of eighteen officials now project a further hike before year-end. The Bank of England held at 3.75% on a 7-2 vote. None of these committees is ready to move on from the energy shock.

- Broadcom's guidance miss mattered: Record quarterly results were punished because AI revenue guidance came in fractionally short of consensus. The AI capex cycle is now being asked to prove its output-side economics.

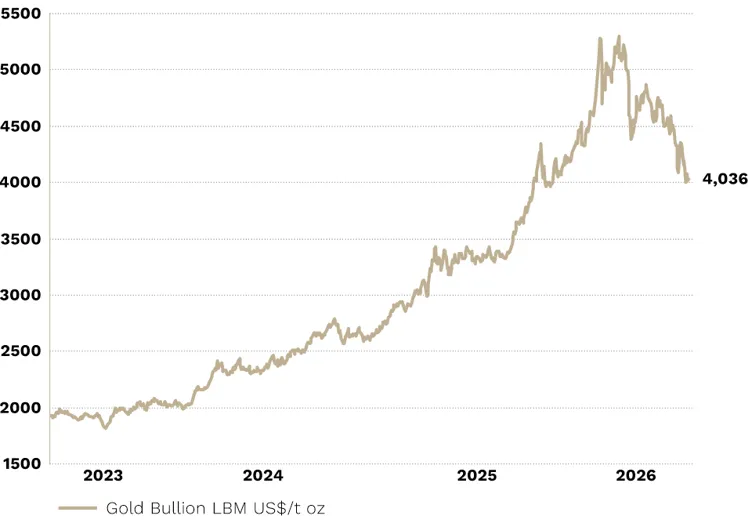

- Gold fell when the dollar debasement thesis met Kevin Warsh: Part of the case for gold rested on the assumption that the Fed would accommodate inflation. Warsh's appointment has challenged that although the fiscal arguments remain unchanged.

- Keir Starmer resigned: The frontrunner to succeed him, Andy Burnham, sat in the Commons only three days after his Makerfield by-election win. Gilt markets were largely unmoved, but a leadership transition adds uncertainty to a fiscal position with little room for error.

Number of vessels passing through the Strait of Hormuz

Source: Apollo, 29 June 2026.